Former Federal Reserve

Chairman Alan Greenspan said that

the financial crisis that triggered our current recession was "by far the greatest financial crisis, globally, ever." That's

right, even worse that the collapse of the stock market in 1929, because for the first time short-term credit was "literally

withdrawn." And with housing starts and car sales till "dead in the water," Greenspan said, we may not see a real recovery

any time soon.

Greenspan is not alone in

his dire pronouncements. Naked Capitalism has a long

list of

economists and bankers who think our current economic crisis could compare to the Great Depression, including current Federal

Reserve Chairman Ben Bernanke, former Federal Reserve Chairman Paul Volcker, Nobel Prize-winning economist Joseph Stiglitz,

and billionaire investor George Soros. While this downturn has not been as painful as the Great Depression, in part because

we avoided some of the policy mistakes we made after the 1929 crash, this economic crisis itself may have been more severe.

And it may take a long time for us to recover.

A large part of the problem is that, as Greenspan says—putting it

mildly—the economic recovery is "extremely unbalanced."

o - the Commerce Department reportedthat January new-home sales dropped 11.2 percent from December,

plunging to their lowest level in nearly 50 years.

o - the Conference Board reported that February consumer confidence fell sharply from January, driven down by the survey's "present situation

index" -- how confident consumers feel right now -- which hit its lowest mark since the 1983 recession...the Reuters/University

of Michigan consumer sentiment survey also showed a falloff from January to February.

o -the Reuters/University

of Michigan consumer sentiment survey also showed a falloff from January to February...the government's report on new jobless claims filed during the previous week shot up 22,000, which was exactly opposite of what economists predicted. Forecasters

expected new jobless claims to drop by about 20,000.

Strauss-Kahn said such an asset could be similar to but distinctly different from the IMF's

special drawing rights, or SDRs, the accounting unit that countries use to hold funds within the IMF. It is based on a basket

of major currencies.

He said having other alternatives to the dollar "would limit the extent to which the international

monetary system as a whole depends on the policies and conditions of a single, albeit dominant, country."

Strauss-Kahn, a former finance minister of France, said that during the recent global financial

crisis, the dollar "played its role as a safe haven" asset, and the current international monetary system demonstrated resilience...

Several countries, including China and Russia, have called for an alternative

to the dollar as a reserve currency and have suggested using the IMF's internal accounting unit.

A secretive group of Wall Street hedge fund bosses are said to be behind

a plot to cash in on the decline of the euro.

Representatives of George Soros's investment business were among an all-star

line up of Wall Street investors at an 'ideas dinner' at a private townhouse in Manhattan, according to reports.

A spokesman for Soros Fund Management said the legendary investor did not

attend the dinner on February 8, but did not deny that his firm was represented.

At the dinner, the speculators are said to have argued that the euro is

likely to plunge in value to parity with the dollar.

The single currency has been under enormous pressure because of Greece's

debt crisis, plus financial worries in Portugal, Italy, Spain and Ireland.

But, it has also struggled because hedge funds have been placing huge bets

on the currency's decline, which could make the speculators hundreds of millions of pounds.

The euro traded at $1.51 in December, but has since fallen to $1.34. Details

of the secretive dinner emerged days after Mr Soros, chairman of Soros

Fund Management, warned in a newspaper article that the euro could 'fall

apart' even if the European Union can agree a deal to shore up support for stricken Greece.

Mr Soros, who made more than $1billion by currency speculation when the pound was ejected from

the Exchange Rate Mechanism on Black Wednesday in 1992, believes the structure of the euro is 'patently flawed'.

The mainstream economics profession is guilty of dereliction of duty. They should be telling

people that this ‘recovery’ is a scam. They should be warning investors that the markets could fall apart any

day. They should be buying gold and selling US Treasuries…and explaining to the politicians that you can’t buy

your way out of a depression with phony dollars squandered on wasteful projects!

Instead, the dopes are patting each other on the back…praising themselves for saving the

planet from destruction...

Prices are vulnerable to sharp, unannounced drops until they finally get down to real depression

levels. Since that hasn’t quite happened yet…we figure it’s still to come.

On the employment front,

this depression has put more than 6 million people out of work. And every month, more people join the unemployment ranks...the

worst thing about a depression is that it holds jobless people prisoner for so long. Many of them will become lifers…they’ll

never work again...

Bank credit is still falling. Households cut back because

they need to get out of debt…and save money for retirement. Businesses cut back too. New projects typically don’t

do well in a depression. Small businesses struggle…and fail. Big businesses get bailouts and subsidies. Depressions

are times to neither a borrower nor a lender be. Debt is only increasing at the government level.

Greece's debt crisis has plunged the euro into a ‘ difficult situation’,

the German Chancellor Angela Merkel admitted last night, prompting fresh fears about the collapse of the single currency.

In the gravest sign yet of the international threat posed by Greece’s

crippled economy, Mrs Merkel warned for the first time that the eurozone faces a ‘ dangerous’ period.

The beleaguered euro initially fell in the wake of her comments and fresh

speculation that Greece’s international credit rating may be downgraded.

On a dramatic day which also saw money markets around the world fall:

The head of Germany’s leading debt management agency warned the euro

would collapse if any member defaulted on its debt.

U.S. regulators said they would investigate whether investment bank Goldman

Sachs helped Athens disguise its budget deficit.

EU inspectors visiting Athens told authorities they see a deeper than

expected recession.

The US is heading for a debt-driven “financial meltdown”

within five to seven years, according to Judd Gregg, the outgoing Republican senator for New Hampshire...Mr

Gregg also complimented China for showing rising alarm about the US’s mounting levels of public debt...“We have had China say that they are looking for other places to put their reservesand

that is probably a smart decision on their part,” said Mr Gregg, who will not seek re-election in November. “So

the warning signs are pretty clear and the path is unsustainable and, at this point, unless we take different actions, unavoidable.”

Secretary of State Hillary Clinton on Thursday said

"outrageous" advice from former Federal Reserve Chairman Alan Greenspan helped create record U.S. budget deficits that put

national security at risk.

Appearing before congressional panels to defend

the State Department's $52.8 billion budget request for 2011, Clinton said the massive U.S. foreign debt had sapped U.S. strength

around the world.

"It breaks my heart that 10 years ago we had a balanced

budget, that we were on the way of paying down the debt of the United States of America," Clinton said.

"I served on the budget committee in the Senate,

and I remember as vividly as if it were yesterday when we had a hearing in which Alan Greenspan came and justified increasing

spending and cutting taxes, saying that we didn't really need to pay down the debt -- outrageous in my view," she said...

Clinton urged lawmakers to tackle the federal budget

deficit, which reached a record $1.4 trillion for the fiscal year that ended last September.

"We have to address this deficit and the debt of

the United States as a matter of national security not only as a matter of economics," Clinton said. "I do not like to be

in a position where the United States is a debtor nation to the extent that we are."

Having to rely on foreign creditors hit "our ability

to protect our security, to manage difficult problems and to show the leadership that we deserve," she said.

Anybody

who looks carefully at the world economy will recognise that a degree of monetary and fiscal stimulus unprecedented in peacetime

is all that is prodding it along, not only in high-income countries, but also in big emerging ones. The conventional wisdom

is that it will also be possible to manage a smooth exit. Nothing seems less likely...

So

what happens next? We can identify two alternatives: success and failure. By “success”, I mean reignition of the

credit engine in high-income deficit countries. So private sector spending surges anew, fiscal deficits shrink and the economy

appears to being going back to normal, at last. By “failure” I mean that the deleveraging continues, private spending

fails to pick up with any real vigour and fiscal deficits remain far bigger, for far longer, than almost anybody now dares

to imagine. This would be post-bubble Japan on a far wider scale.

Unhappily,

the result of what I call success would probably be a still biggerfinancial crisisin future, while

the results of what I call failure would be that the fiscal rope would run out, even though reaching the end might take longer

than worrywarts fear. Yet the big point is that either outcome ultimately leads us to a sovereign debt crisis. This, in turn,

would surely result in defaults, probably via inflation. In essence, stretched balance sheets threaten mass private sector

bankruptcy and a depression, or sovereign bankruptcy and inflation, or some combination of the two....

Most

people hope...that the world will go back to being the way it was. It will not and should not. The essential ingredient of

a successful exit is, instead, to use the huge surpluses of the private sector to fund higher investment, both public and

private, across the world...

With uncharacteristic bluntness, Federal Reserve Chairman Ben S. Bernanke

warned Congress on Wednesday that the United States could soon face a debt crisis like the one in Greece, and declared that

the central bank will not help legislators by printing money to pay for the ballooning federal debt.

Recent events in Europe, where Greece and

other nations with large, unsustainable deficits like the United States are having increasing trouble selling their debt to

investors, show that the U.S. is vulnerable to a sudden reversal of fortunes that would force taxpayers to pay higher interest

rates on the debt, Mr. Bernanke said.

"It's not something that is 10 years away. It affects the markets currently," he told the House

Financial Services Committee. "It is possible that bond markets will become worried about the sustainability [of yearly deficits

over $1 trillion], and we may find ourselves facing higher interest rates even today."

It was some of the toughest rhetoric to date about the nation's fiscal

and budgetary woes from the Fed chief, who faces a second round of questioning Thursday before a Senate panel.

"Now, our first

and most immediate task is to complete the economic recovery by taking additional steps to bolster demand and keep credit

flowing. Along with our efforts to unfreeze credit and stabilize the housing market, the Recovery Act helped to do this, and

it's one of the main reasons our economy has gone from shrinking by 6 percent to growing by nearly 6 percent. But

we need to do more. We should make it easier for small businesses to get loans, and give them a tax credit for hiring new

workers or raising wages.We should invest in infrastructure projects that lead to new jobs in the construction industry and

other hard-hit businesses. And we should provide a tax incentive for large businesses like yours to invest in new plants and

equipment.That would make a difference now. And we need businesses

to support these efforts. ..

At a time of such economic anxiety, it's tempting, and maybe it's easier,

to turn against one another and to find scapegoats to blame. So politicians can rail against Wall Street or against each other,

and businesses can fault Capitol Hill, and all of it makes for easy talking points and good political theater. But it doesn't

solve our problems. It doesn't move us forward. It just traps us in the same debates and divides that have held us back for

a very long time and forced us to keep on punting down the road the same problems we've been facing for decades. And

I believe we can't afford that kind of politics anymore. Not now. But we know the way forward, and we know what the future

can be. And I am confident we can get there. And I'm confident because we have the hardest-working, most productive

citizens in the world. I'm confident because our universities and research facilities are second to none. And I'm confident

because of the caliber of the leaders and businesses represented in this room. We're

not going to agree on every single issue, we're not going to support the same policies every time, but I promise I will never

stop listening to your concerns and your ideas, and I will never stop rooting for your success -- because we are in this together.

And whether we rise or fall as a nation doesn't depend on some economic forces that are beyond our control. It depends on

us -- on the ingenuity of our entrepreneurs, the determination of our workers, and the strength of our people."

Administration officials, independent government analysts and

private forecasters have said the fiscal measures put in place by Democrats have boosted the overall economic growth of the

country and added jobs to the economy.

Still, the need to show economic gains by November is palpable

among Democrats, who are racing to pass additional fiscal measures. The $15 billion package passed in the Senate on Wednesday

would be a modest measure following the $787 billion stimulus package enacted in early 2009.

“We have much more to do to boost employment and put Americans

back to work,” Rep. Carolyn Maloney (D-N.Y.), chairwoman of the Joint Economic Committee, said this week.

The economic risks span the labor market, housing, bank lending

and general concerns about deficits and uncertainty surrounding future regulations.

The

proposal, dubbed the "Volcker rule" after former Federal Reserve Chairman Paul Volcker, would have essentially prevented any

commercial bank with federally insured deposits from owning a division that makes speculative bets with its own capital.

Getty Images

Former Fed Chairman Paul Volcker, left, with Mr. Obama last month.

But

after resistance from lawmakers from both parties, Senate Banking Committee Chairman Christopher Dodd (D., Conn.) and other

legislators are expected to introduce a plan next week that would give regulators more discretion to limit and potentially

ban risky trading at banks, especially if it poses a risk to the broader economy. The measure would stop short of banning

such trading outright.

Former Federal Reserve Chairman Alan

Greenspan said

the financial crisis was “by far” the worst in history and called the recovery from the global recession “extremely

unbalanced.”

The world economy has undergone “by far the greatest

financial crisis globally ever,” Greenspan said today in a speech to the Credit Union National Association’s Governmental

Affairs Conference in Washington.

Greenspan said that while the economy was in worse shape

in the Great Depression, the recent financial crisis was potentially more harmful than that in the 1930s because “never

had short-term credit literally withdrawn.”

Greenspan

said that the gross domestic product may recover to the level of previous peaks earlier this year, even though traditional

drivers of growth such as housing starts and motor vehicles were “dead in the water.” He also said small businesses

show few signs of improving because lenders are struggling with commercial real estate mortgages.

Gradually, people are coming to two contradictory realizations. On the one hand, there really does

seem to be a kind of economic renaissance going on…or, at least that is what you might think if you read the business

and investment news.

On the other hand, people are also coming to realize that we’re in a depression.

...a depression is not just a time when people stand in line to get bowls of soup or sell apples

on street corners. It’s a time of adjustment…when mistakes of the previous boom are corrected…and a new

economic model is found for going forward. This doesn’t happen overnight, no matter how much federal money is put to

work helping it. In fact, the government money just gets in the way…distorting the picture and delaying the necessary

changes. Those black-and-white depression days of the ’30s are gone. Now, we have a depression in full Technicolor…with

plenty of shades of gray, too.

A strengthened U.S. central bank offers the best chance for the U.S. to avoid a future financial crisis, St.

Louis Federal Reserve Bank President James Bullard said Tuesday. "As the lender of last resort, the Fed will be at the

center of any future financial crisis," Bullard said in remarks prepared for delivery to the CFA Virginia Society. He said

that argues for the Fed to play a lead role in financial oversight, reasoning that "provides the nation with the best chance

of avoiding a future crisis."

Bullard criticized financial

overhaul bills drafted in the U.S. House of Representatives and the Senate, both for what they contain and what they omit,

and urged lawmakers to consider changes to give the Fed more information and more authority.

For instance, Bullard questioned whether creation of a financial services oversight council would stave off a

future market meltdown. The idea, contained in the House bill, calls for the Fed to be one of several members of the council,

an approach Bullard said might not work well at a time of crisis when decisions "need to be made quickly, not subjected to

long committee debates."

"The Fed would be better at navigating

this type of decision-making," because of its monetary policy expertise and its political independence, Bullard said.

TheInternational Monetary Fundhas long preached

the virtues of keeping inflation low and allowing money to flow freely across international boundaries. But two recent research

papers by economists at the fund have questioned the soundness of that advice, arguing that slightly higher inflation and

restrictions on capital flows can sometimes help buffer countries from financial turmoil.

1 central banks should set target inflation rate much higher — at 4 percent, rather than the 2 percent standard.

2 officials

“reconsidering the view that unfettered capital flows are a fundamentally benign phenomenon.”

Now

we come to the big dilemma: what if private deleveraging and fiscal deficits continue in the US and elsewhere for years, as

they did in Japan? Then triple A-rated countries, including even the US, might lose all fiscal headroom. This has not yet

happened to Japan. It might well not happen to the US. But it could.

So,

yes, high-income countries face huge fiscal challenges. And yes, the crisis-hit countries start from grossly unsustainable

fiscal positions. But the US is not Greece. Moreover, a massive fiscal tightening today would be a grave error.

There is a huge risk – in my view, a certainty – that this would tip much of the world back into recession. The

private sector must heal. That, not fiscal retrenchment, is the priority.

Even if it handles the current crisis, what about the next one?

It is clear what is needed: more intrusive monitoring and institutional arrangements for conditional assistance. A well-organised

eurobond market would be desirable. The question is whether the political will for these steps can be generated

“Those who argued for deregulation—and

continue to do so in spite of the evident consequences—contend that the costs of regulation exceed the benefits. With

the global budgetary and real costs of this crisis mounting into the trillions of dollars, it’s hard to see how its

advocates can still maintain that position. They argue, however, that the real cost of regulation is the stifling of innovation.

The sad truth is that in America’s financial markets, innovations were directed at circumventing regulations, accounting

standards, and taxation … No wonder then that it is impossible to trace any sustained increase in economic growth (beyond

the bubble to which they contributed) to these financial innovations” - Joseph Stiglitz

.

.

First-hand Perspectives on the Global Economy

In this special report, students from the Joseph H. Lauder Institute of Management & International Studies analyze some

of the most exciting economic, business and technology developments helping to shape today's world.

The articles offer new perspectives on the ever-changing global economy, including the growth

of consumer markets in Brazil, Egypt and China, and the impact of the crisis on French luxury goods. The green economy’s

growth worldwide is captured in articles on organic products in Germany, solar energy in Senegal and Japan’s eco-tech

industry. The rise of the Russian gambling industry, sustainable tourism in Egypt and high-end gastronomy in Spain illustrate

new frontiers in the leisure business. China’s coming of age is captured in articles on the development of its venture

capital and mutual fund industries, enhanced awareness of social corporate responsibility, and the growth of second- and third-tier

cities. New developments in infrastructure and financial services are reflected in pieces on the mobile Internet in Latin

America, the rise to prominence of Spanish infrastructure management companies, and a new form of transparent, customer-driven

banking.

Taken together, the 16 articles offer perspectives on a range of dynamic economies and identify

existing opportunities for conducting business within specific cultural, political and institutional contexts. The articles

are part of the Lauder Global Business Insight program.

Fears are growing that the United States will once again resort to printing money and ginning up inflation to resolve its

debt problem.

While accelerating the

printing presses could do irreversible damage to the dollar's international reputation and the U.S. economy, history suggests

that this is the way Washington will go to avoid the political pain of having to raise taxes and cut spending on popular programs

such as Social Security, defense and Medicare.

Some notable economists

argue that such a move would avert a debt crisis like the one confronting Greece and other European countries that have been

unable to reduce spending because of strong public resistance.

Political leaders and

the Federal Reserve, which is charged with printing and circulating U.S. dollars, strenuously deny that they have any intent

to "inflate" out of the debt...

But despite

some resistance and wariness at the Fed, a growing number of Wall Street gurus expect the U.S. to adopt at least an unofficial

policy of growing or "inflating" out of the debt in light of Congress' unwillingness to tackle budget deficits running at

more than $1 trillion for the foreseeable future.

Economists fear that the nascent recovery will leave more people behind than in past recessions, failing

to create jobs in sufficient numbers to absorb the record-setting ranks of the long-term unemployed.

Call them the new poor: people long accustomed to the comforts of middle-class life who are now relying

on public assistance for the first time in their lives — potentially for years to come.

Yet the social safety net is already showing severe strains. Roughly 2.7 million jobless people will

lose their unemployment check before the end of April unless Congress approves the Obama administration’s proposal to

extend the payments, according to the Labor Department.

States have $18.8 billion of budget gaps yet to

be closed in fiscal 2010. This comes after they have already imposed measures to eliminate budget imbalances totaling $87

billion in the fiscal year, which for most started last summer.

In the budgets they are drafting for fiscal 2011,

states foresee shortfalls of $53.6 billion and for fiscal 2012 $61.6 billion.

The job market isn't improving

as fast as some analysts had expected.

That was the message Thursday in

a government report that the number of people filing first-time claims for unemployment benefits rose unexpectedly last week.

Jobless claims rose by 31,000 to a seasonally adjusted 473,000.

That followed a drop of 41,000

in the previous week. The earlier figure had raised hopes that the job market was improving steadily.

The four-week average for claims

dipped 1,500 to 467,500, near the lows at the end of last year. The average smooths out week-to-week volatility. But many

economists say the four-week average would need to fall consistently below 425,000 to signal that the economy is close to

generating net job gains. The economy has lost 8.4 million jobs since the recession began in December 2007.

Ben Bernanke, chairman of the Federal Reserve, indicated last

week that the central bank might increase its emergency lending rate to banks to widen the spread between that and the main

policy rate. Still, markets were caught off guard Thursday when the Fed raised the discount rate, prompting officials to say

borrowing costs will remain low. "The modifications are not expected to lead to tighter financial conditions for households

and businesses and do not signal any change in the outlook for the economy or for monetary policy," the Fed said

A mortgage crisis like the one that has devastated homeowners is enveloping

the nation's office and retail buildings, and few places are likely to be hit as hard as Washington.

The foreclosure wave is likely to swamp many smaller community

banks across the country, and many well-known properties, including Washington's Mayflower Hotel and the Boulevard at the

Capital Centre in Largo, are at risk, industry analysts say.

The new round of financial pain, which some had anticipated but

hoped to avoid, now seems all but certain. "There's been an enormous bubble in commercial real estate, and it has to come

down," said Elizabeth Warren, chairman of the Congressional Oversight Panel, the watchdog created by Congress to monitor the

financial bailout. "There will be significant bankruptcies among developers and significant failures among community banks."

Bond buyers are thinking about the odds of Greece's debt crisis

spreading to Portugal, Ireland and Spain, then eventually to Britain and the U.S., according to The Economist. While the possibility

of U.S. Treasuries losing their "risk-free" image cannot be rejected, a more likely outcome is higher interest rates on U.K.

and U.S. government debt. "That demands a credible medium-term plan to cut deficits," The Economist notes. "Otherwise Greece's

problems could be the start of something much bigger."

David Rosenberg from Gluskin Sheff

said lending has fallen by over $100bn (£63.8bn) since January, plummeting at an annual rate of 16pc. "Since the credit crisis

began, $740bn of bank credit has evaporated. This is a record 10pc decline," he said. Mr Rosenberg said it is tempting fate

for the Fed to turn off the monetary spigot in such circumstances. "The shrinking in banking sector balance sheets renders

any talk of an exit strategy premature," he said

Paul Ashworth, US economist forCapital Economics,

said that certain Fed officials are clearly worried about lending since they slipped in a warning that bank credit "continues

to contract" in their latest statement..."The reason the Great Depression became 'great'

was the contraction of credit. You would have thought that a student of the Depression like Bernanke would be alarmed by this,"

The number of U.S. workers filing new applications for unemployment insurance

unexpectedly surged last week, while producer prices increased sharply in January, raising potential hurdles for the economic

recovery.

AP

Initial claims for state unemployment benefits increased

31,000 to 473,000, the Labor Department said on Thursday. That compared to market expectations for 430,000.

Another report from the department showed prices

paid at the farm and factory gate rose a faster than expected 1.4 percent from December after a 0.4 percent gain in December,

as higher gasoline prices and unusually cold temperatures helped boost energy costs.

A

bailout of one (nation) will produce the same outcome as the rescue of Bear Stearns did; moral hazard will kick in, and instead

of allowing economic Darwinism to cleanse the gene pool, the weaker nations will lose any incentive to cut spending and trim

their swollen deficits.

Welcome to “Credit Crunch II.”By stuffing billions

of dollars of taxpayers’ money into the balance-sheet holes of the banking industry, governments have transmogrified

private risk into public liabilities.The

“too-big-to-fail” label just reattaches itself to governments from financial companies.

The

sequel, if the European Union or its members are suckered into some kind of Greek rescue package by buying, guaranteeing or

even repaying its bonds, could end up featuringPortugalas Lehman Brothers

Holdings Inc. andSpainas American International Group Inc.

Last year, Russia's economic performance was the worst among the BRIC economies

by a large measure: For the whole of 2009, its real GDP is expected to have declined by at least 8% and some quarters by more

than 10%. That compares to Brazil's smaller real GDP decline of 5.5%, while China's and India's GDPs grew by 8.3% and 6.5%,

respectively. Russia's performance is even worse when compared to 2008, which takes into account the bursting of the oil-price

bubble in the middle of that year.

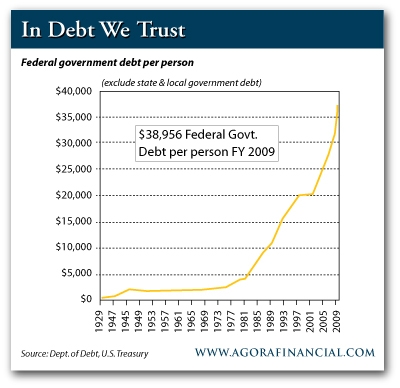

Over the past

year alone, the amount the U.S. government owes its lenders has grown to more than half the country's entire economic output,

or gross domestic product.

Even more

alarming, experts say, is that those figures will climb to an unprecedented 200 percent of GDP by 2038 without a dramatic

shift in course...

"Within 12 years…the

largest item in the federal budget will be interest payments on the national debt," said former U.S. Comptroller General David Walker. "[They are] payments for which we get nothing."

Economic

forecasters say future generations of Americans could have a substantially lower standard of living than their predecessors'

for the first time in the country's history if the debt is not brought under control.

Government debt, which fuels the risk of inflation, could make everyday Americans'

savings worth less. Higher interest rates would make it harder for consumers and businesses to borrow. Wages would remain

stagnant and fewer jobs would be created. The government's ability to cut taxes or provide a safety net would also be weakened,

economists say.

Thomas Hoenig, president of the Federal Reserve Bank of Kansas City, warned:

rising debt...infringing on...central bank’s ability to fulfil...goals

of maintaining pricestability and long-term economic growth.

“Stunning”

deficit projections...putting political

pressure on...Fed to keep interest rates low, infringing on its independence at...risk of inflation

“Without

pre-emptive action, the US risks its next crisis”

the

worst option for the US...a scenario where the government “knocks on the central bank’s door” and asks it

to print more money. Instead, the administration must find ways to cut spending and generate revenue.

If...Fed

succumbed to pressure to increase the money supply...inflation would lead to a loss of confidence in the dollar and in the

economy. Meanwhile, a potential stalemate between the fiscal and monetary authorities that govern the economy could allow

growing imbalances to go unchecked, thus raising the costs of borrowing and of capital for the US.

“dire”

consequences of the central bank prolonging its holdings of mortgage-backed securities, which it purchased in an effort to

prop up the US housing market.

The ongoing Greek financial crisis is the kind of crisis the United States

might face in a few years, if we continue to make the kinds of mistakes that the Greeks have made over the past decade...

aside from our very large budget deficit --9.9 percent of GDP and climbing-- we also have

liabilities that are rarely acknowledged. The costs of Medicare and Medicaid are rising, as is the cost of veterans' care.

Markets assume that the vast debts of Fannie Mae and Freddie Mac are underwritten by the government, and someday the government

might be called upon to pay them. No one is lying about these things, but no one is doing very much about them either.

The good news is that the American government's bankruptcy is not

on the front pages, and it will not be for many years: Our sheer size, our entrepreneurship and our relatively open business

culture will keep us going for a long time. But the Greek crisis shows that the combination of debt and political deadlock

can be deadly.

After decades of warnings that budgetary profligacy, escalating health

care costs and an aging population would lead to a day of fiscal reckoning, economists and the nation’s foreign creditors

say that moment is approaching faster than expected, hastened by a deep recession that cost trillions of dollars in lost tax revenues and higher spending

for safety-net programs...

Many analysts say the president and Congress could send a strong signal

to global markets by agreeing this year to a package of both long-term tax increases and spending reductions, especially in

the popular entitlement programs, that would not take effect until 2012. That is the recommendation of two new studies, one

from a diverse group sponsored by the National Academy of Sciences and a separate joint project of the Peter G. Peterson Foundation, the Pew Charitable Trusts and the Committee for a Responsible Federal Budget.

As debt rises, so do interest costs; by 2014, at a projected $516 billion,

they will exceed the budget for annual appropriations for domestic programs. The government will be competing with the private

sector for credit, forcing interest rates higher and imperiling future prosperity.

Foreign investors now own more than half of the publicly held debt, and

officials for the largest creditor, China, have fretted publicly about the fiscal course of the United States. While few expect

foreigners to dump their assets, since the resulting plunge in values would hurt them as well as everyone else, the fear is

that investors will demand higher interest payments and reduce or stop future debt purchases, threatening the government’s

ability to finance its borrowing.

Lesser financial and fiscal crises have brought the two parties together

to compromise on tough choices about taxes and spending.

A

new joint report from the National Research Council and the National Academy of Public Administration offersU.S.leaders

ways to address the nation's fiscal problems and confront its rapidly growing debt -- a burden that if unchecked will inevitably

limit the nation's future wealth and risk a disruptive fiscal crisis that could lead to a severe recession. The report offers tax and spending options

that would stabilize the debt relative to the size of the economy within a decade.The

report also provides a set of simple tests to determine whether any proposed federal budget would lead to long-term fiscal

stability...The nation's rapidly growing debt now totals more than $12 trillion -- of which

$7.5 trillion is publicly held, about half of it by investors abroad.As

the publicly held debt rises, so does the amount of federal revenue that must be spent on interest payments, leaving less

money for other services and programs.The amount

the government spent on interest was more than $800 per person in 2008 and would roughly double by 2020, even if interest

rates remain at their current low levels.As the debt grows unchecked, so too does the risk

of a crisis; if a loss of investor confidence led interest rates to climb suddenly, the government may be forced into a rushed,

ill-considered response that could deprive people of needed services and hobble the economy for years, the report says.

Marking the anniversary of the $787 billion American Economic Recovery and

Investment Act, Obama aimed his message at people skeptical about the expensive relief measure...

Christina Romer,who heads theWhite House Council of Economic Advisers,said in a separate

interview that one component of the stimulus program had worked especially well. "State fiscal relief really has kept hundreds

of thousands of teachers and firefighters and first responders on the job," she said. "We have seen productivity surge," Romer

said. "And that, at one level, is a good sign out the economy. But absolutely, we've got to translateGDP growthinto employment

growth. Right now, the employmentnumbers look basically stable.

We think we're going to see positivejob growthby spring."

The administration's inspector general: Twenty community agencies that

are slated to receive $45 million are "at risk for fraud, waste and abuse." One example -- Illinois received $242 million

to weatherize 27,000 homes, but the Department of Energy found "significant internal control deficiencies," including one

instance with a "furnace gas leak that could have resulted in serious injury to the occupants."

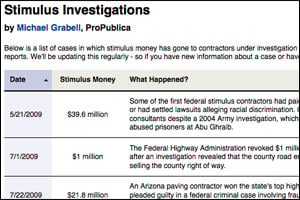

Investigators at ProPublica, which launched a new "Stimulus Investigations"

page, found that billions in stimulus money could be lost to fraud.

"The biggest problem we're seeing is with questionable contractors who

are receiving stimulus funds despite being under criminal investigation. We've seen several examples of this where a contractor

may be banned from getting federal contracts but still is finding a way to get stimulus money."

The

problems faced by the eurozone have cast a long shadow over the markets over the last two weeks. The prospect of a potential sovereign debt default within the single currency area have concentrated

on Greece, but the prospect of similar dangers in Portugal, Ireland and even Spain have rattled investors around the world.

How real is this perceived danger of a sovereign

debt default? What would the consequences be if occurred, and what would be the implication of any EU-sponsored rescue to

avoid one? How should investors position themselves in the face of these risks?

The European Union has

asked Greece to explain reports that it engaged in derivatives trades with US investment banks that may have allowed it to

mask the size of its debt and deficit from EU authorities.Goldman Sachs made up an exchange rate that allowed the Greeks to

look as though they were only engaging in a currency swap when, in effect, they were getting more than a billion more than

they should have from the trades in credit.

The Federal Reserve is scheduled at the end of March to halt its

purchases of mortgage-backed securities, a move that could drive up the low interest rates that have helped the housing market

show new signs of life. The Fed is gambling that private investors will step in to buy the securities, helping to keep rates

from spiking. Senior officials in the Obama administration and at the Fed say they are counting in part on foreigners to keep

the housing market funded.

But financial analysts and advisers familiar with foreign government

funds, known as sovereign wealth funds, predicted that the United States will get limited relief from abroad.

It's logical

to assume that there will be some kind of steps taken after the Chinese New Year to revalue the currency higher. That is probably

at least a few percentage point revaluation of the rate higher against the dollar.

Currency pressure is undermining Chinese influence with it's neighbors

as many struggle to find an export market against a currency undervalued by as much as 40%.

El

sorpresivo aumento de la inflación a través de Latinoamérica en enero generó expectativas de mayores presiones de precios

y puso en evidencia que la era de las tasas históricamente bajas podría terminar antes de lo esperado.

Brasil,

Chile, Colombia y México informaron en las últimas semanas cifras de inflación más sólidas de lo anticipado para enero. En

particular, los analistas sugieren que muchos de los repuntes no son hechos aislados, ya que las cifras de inflación básica

también aumentaron.

The

New York Times revealed that Wall Street’s elaborate financial schemes made Greece escalating debt reach today’s

breaking point by allowing the Greek government to borrow above its means since 2001. One deal created by Goldman Sachs helped

hide billions in debts contracted by Greece from the EU budget authorities in Brussels...

If

The New York Times’ report is confirmed, firms such as Goldman Sachs, which has offices in London, will be in the cross

air of the EU for running financial practices which amount to nothing less than a global elaborate Ponzi scheme, not very

different in nature from the one which got Bernard Madoff behind bars. If the paper’s report is corroborated

by other sources, it is likely that international prosecutions will follow soon against Goldman Sachs’ top executives.

Consumers within the euro zone are not spending enough and the strong

currency is making it hard to tap demand in the rest of the world. The best hope for a home-grown stimulus is Germany, where

firms and consumers had practised thrift when the rest of the world indulged in a spending boom. Sadly Germany still relies

too heavily on exports.

Once a small membership organization

comprisingFannie MaeandFreddie Mac, the mortgage finance giants, and the occasional

troubled auto company, the Future Bailouts of America Club now includes a long list largely populated by financial institutions.

We can’t be sure who the specific members

of this club are — regulators simply say they know ’em when they see ’em. But this much is certain: They’ve

seen a lot of them lately...

“If we are extending

the safety net, extending the implied guarantee to the debts of a lot of other financial institutions, and we know those guarantees

are valuable and costly, then we ought to start budgeting for it. We can’t reduce the costs of these subsidies if we

can’t recognize them.”

Rich countries saw FDI inflows plunge by 41%, and foreign investment

into developing countries fell by more than a third...Despite FDI plunging by 57% last year, America remained the world’s

top investment destination.

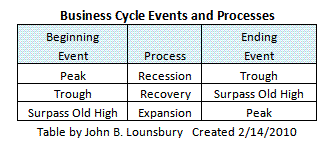

The business cycle is composed

of events and processes. Some descriptions of the business cycle confuse these two things...The business cycle could be much better defined if the recovery and expansion

phases were identified as two individual steps...

They are linked

by an event, the surpassing of the prior peak. The expansion does not begin until new highs are achieved; gains from the trough

simply recover what had been produced in the previous expansion until the prior peak is equaled. The following table shows

these relationships:

The following graph shows the type of illustration that would give a better

representation of the business cycle.

Hace

una década, con sus conocimientos de sofisticados de productos financieros y operaciones con derivados, Wall Street -encabezado

por el mega banco de inversiones estadounidense Goldman Sachs- ayudó a gobiernos europeos como Grecia e Italia a aprovechar

la "contabilidad creativa" con el fin de cumplir con los criterios de convergencia y entrar en la Unión Monetaria Europa.

Ahora, -según se puede desprender de investigaciones en elNew York Times yDer Spiegel- en la primera grave crisis de la zona euro, Wall Street ofrece otros

instrumentos financieros para posponer el coste disparado de la deuda hasta otro dia. Los bancos saben de eso porque es precisamente

la clase de producto financiero de elevada innovación que provocó la primera fase de la crisis global de capitalismo financiero,

el colapso de los mercados de crédito bancario debido a la imposibilidad de medir el riesgo de productos esotéricos financieros

y derivados que nadie entendía. Año y medio después, se transforma en una crisis de deuda soberana.

With theanniversary of the stimulus upon us, politicians are likely tobombard us with numbers: 1.5 million to 2 million jobs created or saved, $272 billion out thedoor,

another $333 billion in the pipeline. The Democratic Policy Committee keeps alist of success storieswhile Sen. Tom Coburn, R-Okla., has publishedtworeportsof 100 “wasteful” projects.

One number that’s been especially hard to pin down: the cost of waste, fraud and abuse.

Already there have been scattered reports about stimulus contractors that are under investigation

or that have had serious violations in their past. Using estimates from fraud experts, the government’s stimulus watchdog,

Earl Devaney, has said as much as $55 billion could be lost.

But no one knows for sure. So to get at the big picture, we at ProPublica decided tostart trackinginspector general reports, auditor

investigations and news accounts about questionable contractors. We’ll be updating our stimulus investigations list

regularly—so if you have new information about a case or one we should add, e-mail it tosuggestions@propublica.org.

VIDEO: Nobel Prize-winning economist Joseph Stiglitz on the Obama administration's economic policies in the midst

of a "sick" economy.

UK Campaign video by Richard Curtis and Bill Nighy,

about the Robin Hood Tax, a tiny tax on bank transactions that could raise hundreds of billions for public services and to

tackle poverty and climate change at home and around the world

MICHAEL SHULMAN

BEST

BOOKS ON THE CRISIS

The Two Trillion Dollar Meltdown -

By far the most powerful book on the crisis because it was written before the real meltdowns rushed to market.

This book should be required reading for every man and woman on Capitol Hill and in the White House for current proposals

on bank reform do nothing to stop the next trillion dollar meltdown - problems in the financial system are very obvious but

are also hidden from most due to their ideological biases and optimism. The author, Charles Morris, is a successful, award

winning financial writer and he outdid himself with a brief book that, among other things, de-mystifies derivatives and their

impact on the financial system. This is the must-read book about the underlying foundation of the crisis.

Too Big To Fail -Almost too big too read, this will probably be viewed as the standard treatment of the crisis due to the clarity

of the writing and the objective stance of the writer, New York Times reporter Andrew Ross Sorkin. Mr. Sorkin does a terrific

job pacing inside the board rooms and with the major players as the crisis unfolds; parts of it almost read like a novel,

but do not let this undermine the credibility of the author or the material. This is a fine overview of who did what and when

to whom. If you have the patience, it is quite good - and if you read multiple books, read it last and you will be able to

skip over some paragraphs here and there.

House of Cards -On one hand, the book is uneven, clearly written in two parts - a contemporary, blow by blow account of the

failure of Bear Stearns and another, the history of the firm. This gives the book an uneven quality that many readers do not

like. So what? The book's mastery of the ten days leading up to J.P. Morgan's (JPM) acquisition of Bear is all you need to read - it is more compelling than many novels I have read and

depicts the behavior of senior executives beyond surreal; for example, during the last week before the fall, the Chairman

refuses to come back to New York because he is playing in a bridge tournament. The book also peeks behind J.P. Morgan's curtain

and that of the New York Fed (Tim Geithner was head of that bank at the time) to show their view of the deal - and better

than anything, shows, day to day, the impact of the derivatives market on share prices and the ability of Bear to borrow money

overnight and continue its operations. A wonderful read, if perhaps too long.

Fool's Gold -Gillian

Tett, a brilliant columnist with the Financial Times, wrote this book on the financial engineers who blew up the financial

world with their invention, the CDO or credit derivative obligation and what we now call credit default swaps. This financial

invention re-defined leverage and when applied to poorly rated RMBS - residential mortgage back securities - well, the world

went boom. Her narrative goes back to the early 1990s and walks the reader through the evolution of the product - explaining

their utility when invented and their decreasing relationship to anything understandable over time as they became more and

more complex and fed the greed of all the players. A wonderful read that, with a little help, could be a novel or a movie.

In Fed We Trust -The second best or must-read by a Wall Street Journal reporter, David Wessel, focuses on Bernanke and the Fed

and how their role unfolded during the crisis. The book has been overlooked - maybe it came out too early - but it is the

best treatment of how various agencies and individuals evolved their thinking and actions during the crisis. What I remember

most from the book is the recurring mantra presented by the author about the actions of the Fed - "whatever it takes" - and

if you accept the facts as presented, as I do, Ben Bernanke will someday be the first face on Mt. Rushmore Two.

On the Brink -Hank Paulson is what the nation now lacks - a hard nosed, savvy, center right Republican leader who views ideology

as an impediment to getting things done. And when in office, understanding the responsibility to get things done, not work

from a playbook. This is a great read - it was the last book I read and it greatly changed my view of Paulson as a man, not

as a Treasury Secretary; if you want one historical treatment of the crisis on your bookshelf, this is it (sorry Mr. Sorkin).

It simply is better at pushing day to day details of the crisis into perspective, juxtaposing them against government policy,

attitudes on Wall Street and so on. And, since I believe what Mr. Paulson wrote, I find him a very appealing public figure,

a leader unlike anyone else in the Bush cabinet, and the right man in the right place at, well, the wrong time for all of

us.

Chain of Blame -This was the most fun book - an inside look at the birth through death of the subprime mortgage industry. The

authors, Paul Muolo and Mathew Padilla, do a great job showing how the mortgage industry ran out of customers so created subprime

mortgages just as Wall Street needed new mortgages to bundle, slice, dice and re-sell. This book brings the reader closest

to how Main Street and Wall Street contributed to the crisis -- Main Street mortgage brokers prompting customers, creating

customers to feed Wall Street's need for products and, alas, commission. An interesting twist in the book is the very positive

treatment of industry poster boy Angelo Mozilo of Countrywide Mortgage (now Bank of America (BAC)). He hated the thought of lending to subprime customers because of the lack of historical data to properly

gauge risk - smart man - but hated giving up market share even worse. The rest is history.

A Colossal Failure of Common Sense -Authors Lawrence G. McDonald and Patrick Robinson do to a bang up job describing the almost surreal behavior

of Lehman Brothers executives as the firm melted down. McDonald is a former Lehman vice president and he focuses on a small

group of executives who pushed Lehman further and further, with leverage, into higher and higher risk positions to generate

profits. The book has prompted some nasty responses - check out some customer reviews on Amazon.com - for it is forceful and

pulls no punches on assigning blame, most it going to Dick Fuld, the CEO of Lehman who comes off poorly in virtually everything

written about the crisis. The value of the book is its ability to portray the gambling mentality that dominated Lehman - a

mentality that led to too much leverage everywhere and is at the very center of the crisis. A very good read, but the book

does not approach the crisis as a whole and is a secondary read if you are trying to get a handle on other things going on

during the crisis apart from Lehman.

It's bad enough that Greece's

debt problems have rattled global financial markets. In the world's largest economic and military power, there's a far more

serious debt dilemma.

For the U.S., the crushing

weight of its debt threatens to overwhelm everything the federal government does, even in the short-term, best-case financial

scenario -- a full recovery and a return to prerecession employment levels..

The U.S. debt crisis also

raises the question of how long the world's leading power can remain its largest borrower.

Moody's Investors Service

recently warned that Washington's credit rating could be in jeopardy if the nation's finances didn't improve.

Despite election-year political

pressure from voters for lawmakers to restrain spending, some recent votes suggests that Congress, left to its own devices,

probably isn't up to the task of trimming deficits.

Claims that the euro could be headed for total collapse are particularly

striking when they come from one of the oldest and largest banks in France - a core founder-member...

In a note to investors, SocGen strategist Albert Edwards said: 'My own view is that there is

little "help" that can be offered by the other eurozone nations other than temporary, confidence-giving "sticking plasters"

before the ultimate denouement: the break-up of the eurozone.'

He added: 'Any "help" given to Greece merely delays the inevitable break-up

of the eurozone.'

The alarming claim came a day after European Union leaders promised 'determined

and co-ordinated' action to shore up Greece's tattered public finances, but disappointed traders by failing to provide specifics...

The French bank's warning was echoed by Mats Persson, Director of the Open

Europe think-tank, which campaigns for reforms in Brussels.

He said: 'The eurozone is facing a fully-fledged crisis. The Greece episode

has made it painfully clear how flawed the euro project was from the very beginning.

'Even if Greece receives a one-off bailout it would not solve the

real problem, which is the huge differences in competitiveness between the eurozone's richest and poorest members. 'If these differences are to be evened out, the EU would need a single budget andcommon taxes so it can redistribute resources...

Harvard University Professor Martin Feldstein, a long-standing sceptic on

the euro, yesterday said the single currency 'isn't working' because member governments have no incentive to keep their public

debts under control. 'There's too much incentive for countries to run up big deficits as there's no feedback until a crisis,'

he said.

Germany drags

EU back towards recession - The eurozone faces

the danger of a 'doubledip' recession after Germany's economy retreated into stagnation.

"If a big non-bank institution gets in trouble and

threatens the whole system, there ought to be some authority that can step in, take over that organization and liquidate it

or merge it -- not save it," Volcker said on CNN.

"It's called euthanasia, not a rescue."

As Congress debates financial reform in the wake

of the worst financial crisis since the 1930s, Volcker has argued for fencing off investment firms primarily engaged in market

speculation from commercial, deposit-taking banks.

With Wall Street’s help, the nation engaged in a decade-long

effort to skirt European debt limits. One deal created byGoldman Sachshelped obscure billions in debt from the budget overseers in Brussels.

Even as the crisis was nearing the flashpoint, banks were searching

for ways to help Greece forestall the day of reckoning.

The U.S. economy is now expected to grow 3% this year and next

-- more than expected a month ago, according to the median estimate of 62 economists polled this month by Bloomberg News. Equally important, those same

economists now expect the U.S. unemployment rate to fall to 9.5% by the end of 2010. The significance of this news? If the

economists surveyed by Bloomberg are accurate about a 3% GDP growth, that would lend credence to Obama administration Council of Economic Advisors Chair Christina Romer's

forecast that the U.S. economy will average monthly job growth of 116,000

jobs per month, or about 1.4 million jobs created in 2010.

Further, if the 1.4 million job forecast

pans out, this will be, arguably, the best economic news Americans have heard in a long time...

Annual investment in public and quasi-public infrastructure systems of 4 to 6 per cent of GDP ($500 - $700 Billion)

will probably be necessary for the foreseeable future but in an era of trillion dollar deficits, no funding source is projected

to have the capacity to generate funds sufficient for infrastructure investment at these levels. At the same time, there is

a clear and immediate need for public and institutional pension funds to invest in instruments that can generate stable, long-term

and low-risk returns on equity.

Theideais that a US

sovereign wealth* fund would dip into public and private pension savings and invest the money in much-needed infrastructure.

If it worked, the economy would benefit, infrastructure would benefit, pensions would receive a healthy return and savings

would be made for the next generation.

“The

core idea of the proposal is to utilize a combination of public and institutional pension funds, individual retirement accounts,

and other private investment capital, together with Social Security Trust Funds to capitalize a National Infrastructure Bank

(NIB) that would provide senior debt to fund projects and programs supported by user fees or other reliable and sustainable

revenue streams.”

Richard G. Little of the University

of Southern California’s School of Policy Planning and Development has an interestingnew paper outentitled,

“Towards a New Federal Role in Infrastructure Investment: Using U.S. Sovereign Wealth to Rebuild America.” The paper’s premise is that the US has to address

years of chronic under-investment in infrastructure. In order to do this, Little want’s to tap into the public

pension and social security savings in order to match long-term investment capital with long-term investments in infrastructure.

So long as this new entity remains commercially oriented, it’s a reasonable

idea; public pension funds have indeed been moving into infrastructure at an increasing rate, driven in large part by the

desire to find assets that better match their long-term liabilities.

Our government has taken extraordinary

steps to head off a feared depression and to stimulate a deflating economy. All well and good. But who has seriously weighed

the unintended consequences of such actions? Where are the long-term forecasts that reflect the consequences of our short-term

remedies? You won't hear answers from the politicians and bureaucrats mainly concerned with staying in office.

A research report by Blanchard and associates at the IMF said policymakers became too complacent during the period

of expansion known as "the Great Moderation" about issues such as inflation and debt. He said that while the financial sector was the source of the recent crisis, "large adverse shocks" could come from

elsewhere in the future such as a pandemic or major terrorist attack. Against

this backdrop, he said aiming for a higher inflation rate could provide more room for policymakers to grapple with crises.

"Maybe policymakers should therefore aim for a higher target inflation

rate in normal times, in order to increase the room for monetary policy to react to such shocks," Blanchard said in a report

"Rethinking Macroeconomic Policy."

In China, the problem isan economy that could be overstimulated. In Europe, it's an economy that could be falling back to sleep.

After expanding at a 0.4% rate in the third quarter of 2009, GDP in the 16-country eurozonegrew by only 0.1%in the year's

last three months. Germany -- the group's largest exporter and biggest economy -- showed zero growth. Economists had been

forecasting a 0.4% fourth-quarter increase, so the drop in growth is fueling speculation that Europe is headed for a double-dip

recession.

As

European leaders grapple with ways to force Greece and other EU debtor nations to live within their economic means, the most

common view among Australian economists is that the debt crisis is not a serious threat to recovery.

Others,

however, say worldwide stimulus measures have simply shifted the private debt problem to government balance sheets, and more

pain is on the way. EU leaders yesterday offered rhetorical support to Greece but no specific aid measures. Prices for equities

and base metals jumped, but markets remain nervous about sovereign debt.

The

International Monetary Fund said this week that the G7 nations owed a combined $US30 trillion ($33.7 trillion).

IMF

managing director Dominique Strauss-Khan said state debt could become the world's "biggest problem for the coming . . . several

years".

Bill Gross, who runs Pimco, one of the world's biggest

bond managers, recently said that he thinks Canada is the best bet for investment among developed nations. "It moved toward

and stayed closer to fiscal balance than any other country," said Gross.

In addition, the Canadian economy, the world's 10th

biggest, is endowed with natural resources increasingly valuable in this century--like potash and uranium. New technologies

allow for the vast development of the Athabasca tar sands in Alberta, helping make Canada's oil reserves the world's second

largest. Yes, there are environmental implications, but Canada is now the biggest supplier of crude oil to the U.S., a lucrative--and

enviable--position for any country.

The population of the People's Republic will be

considerably older than the U.S.' by 2050. It also has far more boys than girls--a rather insidious problem. Among the younger

generation there are already an estimated 24 million more men of marrying age than women. This is not going to end well--except

perhaps for investors in prostitution and pornography.

In the longer term demographic trends actually place

the U.S. in a relatively strong position. By the end of the first half of the 21st century, the American population aged 15

to 64--essentially your economically active cohort--are projected to grow by 42%; China's will shrink by 10%. Comparisons

with other competitors are even larger, with the E.U. shrinking by 25%, Korea by 30% and Japan by a remarkable 44%.

Few thought the second rise would come so soon. Markets were

rattled by fears that the pace of monetary tightening in China would be more aggressive than had been reckoned on, potentially

denting global growth.

“The next five years will see us face another

crunch--the oil crunch. This time, we do have the chance to prepare. The challenge is to use that time well… Our message

to government and businesses is clear: act. Don't let the oil crunch catch us out in the way that the credit crunch did.”

So wrote the CEOs and Chairmen of the companies

involved in the U.K. Industry Taskforce on Peak Oil and Energy

Explosions

of public debt hurt economies in the following way, as numerous empirical studies have shown. By raising fears of default

and/or currency depreciation ahead of actual inflation, they push up real interest rates. Higher real rates, in turn, act

as drag on growth, especially when the private sector is also heavily indebted – as is the case in most western economies,

not least the US.

Although

the US household savings rate has risen since the Great Recession began, it has not risen enough to absorb a trillion dollars

of net Treasury issuance a year.

"The only thing that reliably

grows in our economy is the public debt," Jeffrey D. Sachs writes in a TIME magazine commentary. The government is "utterly

paralyzed" in addressing the issue, Sachs writes, and escalation of the national deficit is leaving the country in a "first-rate

mess." Homeland security, unemployment compensation, and support for state and local governments are only some of the programs

being funded by debt...

When the New Deal deployed deficit spending from 1933 to '36,

the deficits were around 5% of GDP, compared with around 10% today. The publicly held debt was rather stable, around 40% of

GDP then, but it will soon reach 60% of GDP in 2010, and on the Administration's budget plans will rise above 70% by 2012.

What's more, in the 1930s the debt was financed domestically — by Americans. Today about half of public debt is held

by the rest of the world, much of it by China and Japan. In the New Deal era, taxes could easily rise to cover the increased

cost of servicing interest on the debt. Today we have no agreement on how such debt servicing will be paid for. And we face

another unprecedented challenge: large increases in entitlement spending as a share of GDP are likely to continue into the

2020s and '30s as the population ages and health care costs mount...here are the key questions. Will we kill our economic

future by shortchanging the public on investments needed to modernize the economy and train the workforce? Will we borrow

heavily from China and other countries to cover today's spending while racking up massive bills for our children? Or might

we just decide to protect the future of our country through a judicious mix of tax increases and spending cuts that will bring

honor to this generation and prosperity to the next?

More shocking is that banks and their auditors are typically

well aware of the problem, but have not written down the value of property as prices have fallen. Instead they are “extending

and pretending” - or “delaying and praying”: holding property values steady and assisting the borrowers

where possible. They need to. If banks were accurately to record property values, they would write down assets on their own

balance sheets and jeopardise their business...

A very thoroughreportjust released

from the Congressional Oversight Panel expects many banks to go under when the pretence comes to an end. The report concludes:

“There is a commercial real estate crisis on the horizon, and there are no easy solutions to the risks commercial real

estate may pose to the financial system and the public.”

The Fed's strategy hinges on a major shift in its monetary policymaking.

For decades, the central bank has used the federal funds rate as its primary tool for controlling the money supply. Under

the approach outlined by Bernanke, the Fed would take advantage of a relatively new power to pay interest on the funds that

banks keep on reserve with the central bank.

In effect, if banks increase their lending so much that too much

money starts swirling through the economy, raising the risk of inflation, the Fed can increase the interest rate that banks

receive to keep money locked up at the central bank above its current 0.25 percent. That would slow bank lending, keep the

supply of money in check and, Bernanke argued, lead to higher interest rates for all sorts of loans.

The traditional approach to studying economic growth

overlooks the importance of individuals and individual firms.

Market economies are not monolithic – there

are four different types of capitalism (oligarchic, state-guided, big-firm, and entrepreneurial), each with different features

and implications for growth.

Entrepreneurial capitalism is the most effective driver of economic

growth because it provides opportunities for new firms to innovate and create new markets.

Douglas Elmendorf, director of the Congressional Budget Office,

is regarded as an unbiased voice amid partisan budget battles, but the rulings issued by his office often draw ire from lawmakers

on both sides of the aisle. Elmendorf's CBO currently is forecasting big budget deficit increases based on the Obama administration's

proposals...Elmendorf's CBO forecasts that the federal deficit will reach $1.35 trillion this year — $4,400 for every

American. All that red ink means the overall debt will rise to $8.8 trillion by the end of 2010, or about 60% of gross domestic

product — the highest level of public debt since 1952...Now, with the health care plan in deep political trouble, the

focus for both Congress and the White House is shifting from expanding government to shrinking it.

The Great Recession may be over, but this era of high joblessness is probably just beginning. Before

it ends, it will likely change the life course and character of a generation of young adults. It will leave an indelible imprint

on many blue-collar men. It could cripple marriage as an institution in many communities. It may already be plunging many

inner cities into a despair not seen for decades. Ultimately, it is likely to warp our politics, our culture, and the character

of our society for years to come.

One

in five housing markets entered a second leg of home price declines in late 2009, after showing price increases for nearly

half of last year. In 29 of the 143 markets tracked by the site -- including Boston, Atlanta and San Diego -- prices flattened

or began to decrease again in the second part of last year, after five or more months of consecutive monthly increases, according

to the site's fourth quarter real-estate market report...Nationwide, home values fell 5% in

the fourth quarter compared with the fourth quarter a year earlier. Values fell 0.5% from the third quarter of 2009.

While far from representing fixed government

policy, the open demands for retaliation by the PLA officers underscored the domestic pressures on Beijing to deliver on its

threats to punish the Obama administration over the arms sales.

"Our retaliation should not be restricted to

merely military matters, and we should adopt a strategic package of counter-punches covering politics, military affairs, diplomacy

and economics to treat both the symptoms and root cause of this disease," said Luo Yuan, a researcher at the Academy of Military

Sciences...

The warnings from the PLA come

after weeks of strains between Washington and Beijing, who have also been at odds over Internet controls and hacking, trade

and currency quarrels, and President Barack Obama's planned meeting with the Dalai Lama, the exiled Tibetan leader reviled

by China as a "separatist."

The U.S. financial system is

in "much better shape," although small and medium-sized financial institutions are under pressure, which will put a damper

on credit availability in the U.S. economy..."The capital markets are generally open for business--with the important exception

of some securitization markets--and the major securities dealers that survived the crisis have seen a sharp recovery in profitability."

But, "many smaller and medium-sized banks remain under significant pressure," he noted. "Loan losses in commercial real estate

and consumer and mortgage loans seem likely to continue to pressure smaller banks for some time to come," which means "credit

availability to households and small businesses will still be curtailed."

The central bank could keep short-term interest

rates low until 2012 to encourage economic growth, but that it also could use some of its newer monetary tools to check excessive

inflation if it materializes in the current economic recovery...

The

Federal Open Market Committee, which faces tough, unprecedented policy decisions this year as the central bank unwinds first-time

programs it launched during the financial crisis to prevent a second Great Depression.

The programs include “quantitative easing”

measures designed to help keep interest rates low and to pump ready cash – liquidity – into the financial system.

The “QE” supplemented the FOMC’s principal policy mechanism: setting the Federal Funds rate, the short-term

benchmark interest rate banks charge each other for overnight borrowing.

At the height of the crisis, the FOMC cut the

Fed Funds rate to about zero, where they remain today; a reversal now could rattle fragile financial markets still on the

mend.

What you’re not hearing from the politicians and the talking

heads is that the joblessness and underemployment in America’s low-income households rival their heights in the Great

Depression of the 1930s — and in some instances are worse. The same holds true for some categories of blue-collar workers.

Anyone who thinks this devastating problem is going away soon, or that the economy can be put back on track without addressing

it, is deluded.

There has been talk about income inequality over the past several

years, but what is happening now is catastrophic...the lowest group, which had annual household incomes of $12,499 or less...unemployment rate during the fourth

quarter of last year was a staggering 30.8 percent. That’s more than five points higher than the overall jobless rate

at the height of the Depression.

The next lowest group, with incomes of $12,500 to $20,000, had

an unemployment rate of 19.1 percent.

These are the kinds of jobless rates that push families already

struggling on meager incomes into destitution. And such gruesome gaps in the condition of groups at the top and bottom of

the economic ladder are unmistakable signs of impending societal instability.

Greenspan added that, as many economists agree, the economic

recovery will have to continue for some time to absorb the slack in the labor force to lower the U.S. unemployment rate significantly.

Greenspan then agreed with co-guest former U.S.

Treasury Secretary Henry Paulson that one key to job growth would be a longstanding characteristic of the historically adaptable,

resilient U.S. economy: innovation. That's the rate at which new businesses are formed, and existing businesses deploy new

technologies/products/services, and find ways to operate more efficiently.

The $2.8 trillion municipal bond market is likely to crash in

the same way as the markets for housing and technology, said Michael Aronstein of Marketfield Fund. Politicians have taken

advantage of the low cost of credit to pile up an unsustainable level of debt, Aronstein said. "I think we're getting quite

close," Aronstein said. "You'll see people trying to withdraw money from the municipal bond funds. The big risk comes when

you start seeing the tightening credit cycle."

As the United States and Europe deal with economic contraction resulting from excessive credit expansion that

many believe has lead to another Great Depression, China’s future remains hazy. Some argue that China has replaced the