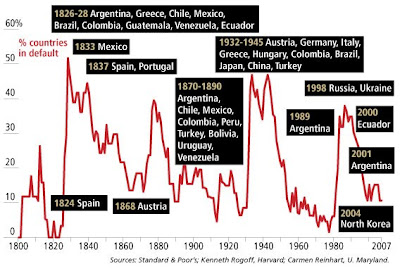

"Sovereign defaults--when a country stops paying its bills--go in waves, often following global financial crises, wars

or the boom-bust cycles of commodities. Some countries, like Spain and Austria, mend their ways; others, like Argentina, are

repeat offenders. The combination can be fatal for investors holding bonds issued by financially shaky countries like Argentina

or Greece, which sell a lot of their debt outside their own borders (as does the U.S.--45% of all publicly held debt). As

a nation's finances deteriorate, foreign investors sell their bonds, putting upward pressure on interest rates. That usually

sets off a spiral including a deteriorating currency, which, if the bonds are denominated in foreign currencies, makes it

impossible for the country to pay its debt."

Hammered by Republicans for billions of dollars in spending that added

to the deficit, Obama outlined steps he said would rein in spending. They include rules requiring that spending or tax cuts

be offset by cuts to other programs or tax increases, a freeze on most discretionary spending and a presidentially appointed

commission to recommend ways to reduce the deficit.

Economists are encouraged that business investments appear to be coming

back even though the job market continues to drag. New U.S. Commerce Department data shows orders for durable goods, not including

transportation equipment, rose 0.9% in December, surpassing forecasts. The Labor Department reported that weekly unemployment

applications fell to 470,000 in the week ending Jan. 23, exceeding the median estimate of 450,000 predicted by 42 economists

polled by Bloomberg.

“A strong, healthy financial market makes it possible

for businesses to access credit and create new jobs. It channels the savings of families into investments that raise

incomes. And that can only happen if we guard against the same recklessness that nearly brought down our entire economy.” Essential

reforms include measures to protect consumers and investors from financial abuse; close loopholes, raise standards, and create

accountability for supervision of major financial firms; restrict the size and scope of financial institutions to reign in

excesses and protect taxpayers and address the ‘too big to fail’ problem; and establish comprehensive supervision

of financial markets.

So, what did we get for all that dough? Unfortunately, more questions than answers.Indeed, many of the factors that helped cause the previous crisis -- a sustained period of low

interest rates, high levels of consumer debt in the West and excessive risk-taking by financial institutions -- remain in

place. Atthe same time, supersized government

bailouts could have created the conditions for future financial crises that will be larger and even more expensive than the

one the world has just suffered. Despite the protestations

by politicians that such a large-scale rescue should never be allowed to happen again, their actions over the past two years

suggest the opposite...For central bankers, politicians and policymakers...the challenges are immense.

They must withdraw the financial support that has been provided to the financial sector without triggering a collapse, but

before new risk-taking creates the conditions for another collapse. They must overhaul regulation to make banks safer while

reversing the moral hazard that has characterized the current round of bailouts. They must manage a controlled

reduction of government debt. And they must attempt to rebalance the world economy without withdrawing into conflict and protectionism.

There is little doubt that the authorities' swift response to

the crisis prevented an even more severe economic collapse. But the global financial system is far from being fixed.

The global economic recovery could lose pace later this year, dashing

hopes for a rapid escape from the deepest downturn of the postwar era, economists and investors said at the World Economic

Forum's annual meeting

Markets are ultimately about people, which is what George Akerlof and

Robert Shiller talk about in Animal Spirits: How Human Psychology Drives the Economy, and Why It Matters For Global Capitalism

(Princeton University Press, £16.95). It deals with that relatively new field, “behavioural economics”, or

how the economy really works. As they put it in the Introduction, “it accounts for how it works when people really are

human, that is, possessed of all-too-human animal spirits”, or human frailties.

According to the authors, there are five ways in which “animal spirits”

manifest themselves in economic behaviour:

The state of the economy depends upon the “feel-good” factor

or the level of confidence about how the future will pan out. This is not a rational prediction but based on instinct, which

is the most crucial feature of “animal spirits”.

A sense of fairness can overrule rational economic motivations. For example,

the demand for shovels can rise after a snowstorm, but raising prices at such a juncture would be considered unjust by the

majority and, therefore, desisted.

The action of monopoly capitalism — multinationals or predatory

corporations can impact the entire economy. For instance, the actions of energy giant Enron led many to lose faith in financial

markets as a whole.

Many people make their economic decisions without taking into account

inflation: instead of maximising their real (inflation-adjusted) income, they succumb to “money illusion”.

Finally, human behaviour is heavily influenced by stories and narratives

with logic that drive people to action. We’re all gullible idiots at the time and only later wake up to realise we’ve

been conned.

If you put all the five factors together, the conclusion is obvious: “animal

spirit” forces other than reason guide our actions. If you look back, none of them are based on rational grounds and

this “irrationality” must be taken into account to understand how economies actually work. If economists have

failed to explain repeated crises, it is because they have interpreted economic activity through an unreal model. Economists

have based their studies on mathematical models of human behaviour whereas they should have been based on human psychology

and practical politics of the times.

The global recovery is off to a stronger start than anticipated earlier but is proceeding at different

speeds in the various regions. Following the deepest global downturn in recent history, economic growth solidified and

broadened to advanced economies in the second half of 2009. In 2010, world output is expected to rise by 4 percent. This represents

an upward revision of ¾ percentage point from the October 2009 World Economic Outlook. In most advanced economies, the recovery

is expected to remain sluggish by past standards, whereas in many emerging and developing economies, activity is expected

to be relatively vigorous, largely driven by buoyant internal demand. Policies need to foster a rebalancing of global demand,

remaining supportive where recoveries are not yet well sustained.

Leading experts brought together by the

World Economic Forum developed proposals to help tackle corruption. Their reportRaising Our Game: Next Steps for Business, Government and

Civil Society to Fight Corruptionrecommends

the following: • For Businesses– empower

ethics officers to prevent bribery through anti-corruption programmes, such as the Partnering Against Corruption Initiative

(PACI) • For Governments– create a level

playing field by ratifying and fully implementing the United Nations Convention Against Corruption into national law • For

Civil Society– strengthen its “watchdog” role to

promote ethical practices with business and government

The rapid expansion of

the European Union in the past decade parallels that of the United States just before the Civil War. In both cases, the unions

seemed strong until the economic environment soured. Could the EU be headed for a civil war?

Perhaps not war, but “divorce”

(civil or otherwise) may be imminent for Europe, claims the Socionomic Institute.

“Both unions appeared

to be strong when markets were rising. But once stocks reversed, the stress of a bear market severed those bonds quickly,”

explains study author Brian Whitmer, editor of Elliott Wave International’s EUROPEAN FINANCIAL FORECAST. “War

eventually broke out among the U.S. states, and I believe that an equally perilous period is coming for the countries of the

EU.”

Thinking of counting to a trillion

one second per number? Better get started. It will take 31,688 years.

And tack on a few more years if

you want to go for 1.35 trillion, the dollar estimate for the federal deficit in the current budget year.

The whole sum could be taken care

of if every American, all 300 million of them, forked over $4,500.

Back in 1981, President Ronald

Reagan, characterizing the national debt as it approached $1 trillion, commented that "a trillion dollars would be a stack

of $1,000 bills 67 miles high." The debt, the accumulation of annual deficits, now stands at more than $12 trillion.

Put another way, the $1.35 trillion

could pay for 40,000 players like Alex Rodriguez, whose $33 million salary in 2009 made him baseball's richest man.

Or think the $6.25 billion paid

out by Goldman Sachs in salaries and bonuses in 2009 was a lot of money? The federal deficit could support the payroll of

216 such financial firms.

A trip around the world at the

equator is about 25,000 miles. So 1.35 trillion miles would be a dizzying 54 million circuits around the globe.

A trillion is one followed by 12

zeros.

The Washington Monument, overlooking

the deficit debate in the Capitol, stands about 555 feet high. Stacked end to end, it would take more than 2.4 billion monuments

to reach 1.35 trillion feet. That's well more than double the distance from the Earth to the sun.

Being sat on by a 10,000-pound

bull elephant would be a crushing experience. What about if 135 million pachyderms were piled up?

The Earth has been around for about

4.5 billion years. A long time until you consider that 1.35 trillion years equals 300 Earth lives. Looking at more modern

history, 1.35 trillion seconds would take us back more than 40,000 years, when Neanderthals were using stones to make tools.

By Jim Abrams ASSOCIATED

PRESS in The Washington Times

.

What Is Wrong With the Job MarketAnd

How to Fix It

CONCLUSION: The Great Recession is over, but the recovery will be a difficult

slog through much of this year. The risks are also uncomfortably high that the economy will backtrack into recession. This

would be an especially dark scenario, almost certainly involving a deflationary spiral of falling wages and prices. The Federal

Reserve and fiscal policymakers would also have fewer options and resources with which to respond.

A range of problems suggest that such a scenario cannot be easily dismissed.

Most obvious are high and rising unemployment and weak wage growth, the mounting foreclosure crisis, rising commercial mortgage

loan defaults and resulting small bank failures, budget problems at state and local governments, and dysfunctional structured-finance

markets that restrict credit to consumers and businesses.

Policymakers should provide more help to the economy to ensure the recovery

becomes self-sustaining. The Federal Reserve must not raise interest rates too soon or end its credit easing efforts too quickly.

Congress must provide more resources to unemployed workers whose benefits are running out, to state governments unable to

balance their budgets, and to small businesses looking for credit and all businesses that expand payrolls.

All this help comes at significant cost. While the fiscal stimulus has

been vital, it has helped produce a $1.4 trillion budget deficit this past fiscal year and will lead to another similarly

sized deficit in the current one. Yet the cost to taxpayers would have been measurably greater if policymakers had not acted

aggressively. The recession would still be in full swing, undermining tax revenues and driving up government spending on Medicaid,

welfare, and other income support for distressed families.

It is a tragedy that the nation has been forced to spend so much to tame

the financial crisis and end the Great Recession. Yet it has been money well spent.

The Budget and Economic Outlook: Fiscal Years 2010 to 2020

January 2010

The Congressional Budget Office projects that

if current laws and policies remained unchanged, the federal budget would show a deficit of $1.3 trillion for fiscal year

2010. That amount would be slightly smaller than the 2009 deficit but, as a share of the economy as a whole (measured by gross

domestic product, or GDP), it would still be the second largest since World War II. The budget picture remains daunting beyond

this year, with deficits averaging about $600 billion annually from 2011 through 2020.

Those estimates are not intended to be a prediction

of actual budget outcomes; rather, they indicate what CBO estimates would occur if current laws and policies remained in place.

Toward that end, CBO’s projections presume no changes in current tax laws or spending programs. Any new legislation

that reduced revenues (such as indexing the alternative minimum tax for inflation) or boosted spending (such as providing

supplemental funding for military operations in Afghanistan) would increase projected deficits. For example, if all tax provisions

that are scheduled to expire in the coming decade were extended and the AMT were indexed for inflation, deficits over the

2011–2020 period would be more than $7 trillion higher. (See the above chart for details on the budgetary impact of

some alternative policy actions and see the sidebar for more information on CBO’s baseline.)

Accumulating deficits are pushing federal

debt to significantly higher levels. CBO projects that total debt will reach $8.8 trillion by the end of 2010. At 60 percent

of GDP, that would be the highest level since 1952. Under current laws and policies, CBO’s projections show that level

climbing to 67 percent by 2020. As a result, interest payments on the debt are poised to skyrocket; the government’s

spending on net interest will triple between 2010 and 2020, increasing from $207 billion to $723 billion.

Economic growth will probably remain muted

for the next few years. The deep recession that began in 2007 appears to have ended in the middle of 2009. The economy grew

during the third quarter, and early signs suggest that the labor market strengthened slightly late in 2009. CBO expects that

the economy will continue to grow, although at a slower pace than in past recoveries. Hiring rates remain very low, and CBO

projects that the unemployment rate will average more than 10 percent during the first half of 2010, before beginning a gradual

decline. That pattern is typical of recent recessions, where hiring continues to fall for 6 to 12 months after the economy

begins to grow.

Beyond the 10-year projection period, growth

of spending for Medicare, Medicaid, and Social Security will speed up from its already rapid rate. To keep federal deficits

and debt from reaching levels that would substantially harm the economy, lawmakers would have to significantly increase revenues,

decrease projected spending, or enact some combination of the two.

DAVOS

DATOS

Bubblechology

Robert J. Shiller, a well-known Yale economist, suggested that bubbles

could be diagnosed using the same methodology psychologists use to diagnose mental illness.

After all, a bubble is a form of psychological malfunction. And like mental

illness there’s a tricky gray area between being really sick and just having a few problems, Shiller said during a panel

discussion at the World Economic Forum in Davos, Switzerland.

The solution: a checklist like psychologists use to determine if someone

is suffering from, say, depression. So here is Shiller’s checklist.

Sharp increases in the price of an asset such as real estate or dot-com

shares

Great public excitement about said increases

An accompanying media frenzy

Stories of people earning a lot of money, causing envy among people who

aren’t

Growing interest in the asset class among the general public

“New era” theories to justify unprecedented price increases

A decline in lending standards

DAVID M. WALKER

EX-COMPTROLLER

GENERAL OF THE US

Political timidity invites financial disaster

In his State of the Union address, President Obama noted that "campaign fever has come

even earlier than usual" this year. Indeed it has. Typically, politicians in campaign mode make big, expensive promises to

voters - new programs, new benefits, new and bigger tax cuts. We will surely see some of that this year; but what is notable

about the conversation in Washington right now - and on the campaign trail - is its focus on deficits and debt. The White

House and members of both parties appear to see political advantage in talking about fiscal discipline. That's a good thing,

but only if they take action - serious action - soon.

America, simply put, is not on a sustainable path. Within two decades, if we haven't dramatically changed the way

we do business in Washington, we'll either see critical social programs going bankrupt, or our tax rates doubling to cover

the shortfall. The dysfunction is not only fiscal but cultural; it is rooted deeply in our political system.

In fact, there are at least four disturbing parallels between the factors related to the recent subprime mortgage

crisis that caused the recession, and the actions of the federal government, which may cause the next financial crisis.

First, consider the chasm between those who bear the burdens of financial risk-taking and those who reap the benefits.

During the subprime mortgage crisis, the people who sold unsound mortgages weren't the same people who held them. Now the

bankers are back in the black, and homeowners are still paying the price. So are the taxpayers.

But is that practice really so different than that of elected leaders who increase spending and cut taxes while

refusing to consider the long-term costs of either? Today's politicians reap short-term, electoral gains; tomorrow's taxpayers

get a long-term, crushing obligation.

Second, remember how impenetrably complicated the subprime securities were? They were almost impossible to explain

to anyone outside the big banks - even to many inside players, as well. That lack of transparency fueled the illusion that

the economy was sound instead of on the brink.

This is uncomfortably similar to the way the government handles its finances. We all know that the federal budget

deficit has spiraled out of control. But fewer people are aware that those annual deficits are understated. If you think the

$12.3 trillion national debt is too high, the federal government has tens of trillions of obligations, commitments and contingencies

that aren't on the federal balance sheet.

Third, most of the corporations crippled by the subprime crisis paid little or no attention to the danger signs,

which included mounting debt, dwindling cash flow and unrealistic credit ratings.

It reminds me of our federal government's cavalier attitude toward debt. By the end of fiscal year 2010, we will

have a total debt approaching 95 percent of our economy - and half of the public debt is held by foreign lenders. To put this

in historical perspective, our Founding Fathers took on debt at a level of 40 percent of the economy to win our independence

and gain agreement on the U.S. Constitution. And at the end of World War II, though we had debt equal to 122 percent of our

economy, we had virtually no foreign debt. There is simply no precedent for today's type of indebtedness.

Fourth, and most important of all, recall how major corporations failed to address the growing risks of the housing

bubble before it burst into a full-blown crisis. Risk managers failed to adequately anticipate the disaster scenario for housing

prices. Corporate overseers, including boards of directors, did an inadequate job of monitoring related risks.

Is that so different than the government's own lax vigilance? Federal regulators allowed too many players on the

field with too few referees. Deregulation led to a general weakening of standards for transparency, accountability and oversight.

When the crisis hit, the government was caught completely off step - and hardly seems to have regained its footing.

As we enter a new decade, and our economy begins to recover, let us hope that our national leaders will take a

step back, recognize the depths of our long-term fiscal challenges and start making the hard choices to avoid the next crisis.

So far, the signs are mixed. A group of senators succumbed to pressure from the extreme right and left and effectively

killed the creation of a commission that would have recommended changes in fiscal policy. Conservatives feared its authority

to raise taxes; progressives feared its authority to cut spending. That's not a promising start. Still, it is encouraging

that a majority of senators favor the idea, and so does the president. As he just announced in his State of the Union address,

he is prepared to establish such a commission by executive order.

Politicians of both parties frequently say that those who caused the nation's economic crisis - by this they mean

Wall Street bankers - need to change the way they do business. In equal measure, that should apply to Washington, too.

David M. Walker is president and CEO of the Peter G. Peterson Foundation, former

comptroller general of the United States (1998-2008) and author of "Comeback America" (January 2010)

CBO DIRECTOR TO CONGRESS: "...accumulating deficits will push federal debt held by the public to significantly

higher levels. At the end of 2009, debt held by the public was $7.5 trillion, or 53 percent of GDP; by the end of 2020, debt

is projected to climb to $15 trillion, or 67 percent of GDP. With such a large increase in debt, plus an expected increase

in interest rates as the economic recovery strengthens, interest payments on the debt are poised to skyrocket. CBO projects

that the government’s annual spending on net interest will more than triple between 2010 and 2020 in nominal terms,

from $207 billion to $723 billion, and will more than double as a share of GDP, from 1.4 percent to 3.2 percent..."

UNEMPLOYMENT RATE

CBO projects, that if current

laws and policies remained unchanged, the federal budget would show a deficit of $1.3 trillion for fiscal year 2010. At 9.2

percent of gross domestic product (GDP), that deficit would be slightly smaller than the shortfall of 9.9 percent of GDP ($1.4

trillion) posted in 2009. Last year's deficit was the largest as a share of GDP since the end of World War II, and the deficit

expected for 2010 would be the second largest. Moreover, if legislation is enacted in the next several months that either

boosts spending or reduces revenues, the 2010 deficit could equal or exceed last year's shortfall.

The

world economic recovery will speed up, the dollar will strengthen and equities and profits improve, according to a panel of

leading experts on Wednesday.

Despite further

consolidation in economic and financial systems and continued volatility in global markets, 2009 was "a year that showed the

first sign of regained optimism and confidence in financial markets," said John Prestbo, editor and executive director of

Dow Jones Indexes, which organized the 2010 Global Economic Outlook panel discussion.

A shift in market sentiment has led to more optimistic forecasts for economic growth.

"Two years after the start of a severe worldwide

recession, a rebound in global economic activity is clearly underway with industrial production and international trade flows

rising briskly," said Kevin Logan, an independent global economist. "By the middle of this year, estimates for global GDP

growth in 2010 are likely to be double what they were in the middle of 2009."

President Obama's plan to restrict banks from making speculative investments is seen as one of his

boldest financial reforms. This Backgrounder reviews the government's regulatory proposals and the debate over their long-term

impact.

The Federal Reserve plans to stop buying securities issued by government housing loan agencies Fannie

Mae and Freddie Mac by the end of the first quarter. This is not only likely to push up mortgage rates; Treasury rates should

rise as well. Throughout 2009, the private sector sold a portion of their agency holdings to the Fed and used those funds

to buy Treasurys. Once the Fed’s agency purchases stop, this private sector portfolio shift will end, removing a major

source of demand in the Treasury market. As the chart shows, since the start of 2009 the Fed has bought or financed the entire

increase in Treasury issuance. As Fed purchases slow and Treasury issuance continues at a high level, interest rates will

have to move up to attract new buyers.

CHINA LENDING TO U.S.

January

22, 2010

Debt

Burden Now Rests More on U.S. Shoulders

THE

United States government borrowed more money than ever before in 2009, but its largest lender — China — sharply

reduced the amount it was willing to lend.

The United States Treasury estimated

this week that during the first 11 months of last year China raised its holdings ofTreasury securitiesby

just $62 billion. That was less than 5 percent of the money theTreasuryhad to raise.

That raised its holdings to $790 billion,

leaving it the largest foreign holder of Treasury securities — Japan is second at $757 billion and Britain a distant

third at $278 billion. But China’s holdings at the end of November were lower than they were at the end of July.

Not since 2001, when China was still a relatively

minor investor in Treasury securities, had the country shown a decline in holdings over a six-month period.

President Obama: "Never

Again Will the American Taxpayer be Held Hostage by a Bank that is 'Too Big to Fail'"

From the White House

The President proposed what he called "the Volcker Rule," named after

one of the fiercest advocates for financial reform over the past year, and who has been particularly focused on addressing

the issue of banks being "too big to fail." He also proposed addressing one of the clearest issues leading to the financial

crisis of the past years, namely banks that stray wildly from their core mission: serving their customer. Having met

with Paul Volcker this morning, and having last week proposed new fees on Wall Street to ensure the taxpayersget their money back, thePresident came with a direct message for banksthat might object to these changes:

I welcome constructive input from folks in the financial

sector. But what we've seen so far, in recent weeks, is an army of industry lobbyists from Wall Street descending on

Capitol Hill to try and block basic and common-sense rules of the road that would protect our economy and the American people.

So if these folks want a fight, it's a fight I'm ready

to have. And my resolve is only strengthened when I see a return to old practices at some of the very firms fighting

reform; and when I see soaring profits and obscene bonuses at some of the very firms claiming that they can't lend more to

small business, they can't keep credit card rates low, they can't pay a fee to refund taxpayers for the bailout without passing

on the cost to shareholders or customers -- that's the claims they're making. It's exactly this kind of irresponsibility

that makes clear reform is necessary.

President Barack Obama meets with Economic Recovery Advisory Board Chair Paul Volcker in

the Oval Office January 21, 2010. (Official White House Photo by Pete Souza)

The President went on to explain the reforms he was proposing in more

detail:

First, we should no longer allow banks to stray too

far from their central mission of serving their customers. In recent years, too many financial firms have put taxpayer

money at risk by operating hedge funds and private equity funds and making riskier investments to reap a quick reward.

And these firms have taken these risks while benefiting from special financial privileges that are reserved only for banks.

Our government provides deposit insurance and other

safeguards and guarantees to firms that operate banks. We do so because a stable and reliable banking system promotes

sustained growth, and because we learned how dangerous the failure of that system can be during the Great Depression.

But these privileges were not created to bestow banks

operating hedge funds or private equity funds with an unfair advantage. When banks benefit from the safety net that

taxpayers provide –- which includes lower-cost capital –- it is not appropriate for them to turn around and use

that cheap money to trade for profit. And that is especially true when this kind of trading often puts banks in direct

conflict with their customers' interests.

The fact is, these kinds of trading operations can create

enormous and costly risks, endangering the entire bank if things go wrong. We simply cannot accept a system in which

hedge funds or private equity firms inside banks can place huge, risky bets that are subsidized by taxpayers and that could

pose a conflict of interest. And we cannot accept a system in which shareholders make money on these operations if the

bank wins but taxpayers foot the bill if the bank loses.

The proposal would:

1. Limit the Scope - The President

and his economic team will work with Congress to ensure that no bank or financial institution that contains a bank will own,

invest in or sponsor a hedge fund or a private equity fund, or proprietary trading operations unrelated to serving customers

for its own profit.

2. Limit the Size - The President

also announced a new proposal to limit the consolidation of our financial sector. The President’s proposal will

place broader limits on the excessive growth of the market share of liabilities at the largest financial firms, to supplement

existing caps on the market share of deposits.

In the coming weeks, the President will continue

to work closely with Chairman Dodd and others to craft a strong, comprehensive financial reform bill that puts in place common

sense rules of the road and robust safeguards for the benefit of consumers, closes loopholes, and ends the mentality of “Too

Big to Fail.” Chairman Barney Frank’s financial reform legislation, which passed the House in December,

laid the groundwork for this policy by authorizing regulators to restrict or prohibit large firms from engaging in excessively

risky activities.

As part of the previously announced reform program,

the proposals announced today will help put an end to the risky practices that contributed significantly to the financial

crisis.

The rise in joblessness was a sharp change from November, when 36

states said their unemployment rates fell...The rise

in joblessness was a sharp change from November, when 36 states said their unemployment rates fell...Nationally, more than 600,000

people left the labor force in December, according to government data. The large exodus from the labor force indicates that

"unemployment is a lot worsethan the numbers suggest"...

Developing countries facing higher borrowing costs,

lower credit levels, and reduced international capital flows

The global economic recovery that is now underway will slow later this year

as the impact of fiscal stimulus wanes. Financial markets remain troubled and private sector demand lags amid high unemployment,

according to a new report from the World Bank.

Global Economic Prospects 2010, released today, warns

that while the worst of the financial crisis may be over, the global recovery is fragile. It predicts that the fallout from

the crisis will change the landscape for finance and growth over the next 10 years.

Global GDP, which declined by 2.2 percent in 2009, is expected to grow 2.7 percent

this year and 3.2 percent in 2011[1].Prospects

for developing countries are for a relatively robust recovery, growing 5.2 percent this year and 5.8 percent in 2011 -- up

from 1.2 percent in 2009.GDP in rich countries, which declined

by 3.3 percent in 2009, is expected to increase much less quickly—by 1.8 and 2.3 percent in 2010 and 2011. World trade

volumes, which fell by a staggering 14.4 percent in 2009, are projected to expand by 4.3 and 6.2 percent this year and in

2011...

Stronger

fundamentals helped theLatin America and the Caribbeanregion

weather this crisis much better than in the past. Following an estimated 2.6 percent drop in GDP last year, regional output

is projected to increase by 3.1 percent in 2010 and 3.6 percent in 2011, but weaker investment will keep growth from attaining

boom year levels. Remittances and to some extent tourism (both important sources of external finance for Caribbean countries)

are expected to recover only modestly in the 2010–11 period, undermined by weak labor market conditions in the United

States and other high-income countries. Key challenges include the winding down of stimulus measures; providing for the unemployed

in a fiscally sustainable manner; and maintaining openness towards international trade and investment.

$1.900,000,000,000 increase in US debt limit proposed

Senate Democrats...proposed allowing the federal government

to borrow an additional $1.9 trillion to pay its bills, a record increase that would permit the national

debt to reach $14.3 trillion. The unpopular legislation is needed to allow the federal government to issue

bonds to fund programs and prevent a first-time default on obligations.

The record increase in the so-called debt

limit is required because thebudget deficithas spiraled out of

control in the wake of a recession that cuttax

revenues, theWall

Street bailout, and increased spending by the Democratic-controlled Congress. Last year's deficit hit a phenomenal

$1.4 trillion, and the current year's deficit promises to be as high or higher...Less than a decade ago, $1.9 trillion

wouldhave been enough to finance theoperations

and programs of the federal government for an entire year.

The UK government expects borrowing to come in at £178

billion this year, topping 12% of gross domestic product, but has pledged to halve its deficit over the next four years.

Recorded history covers much less than one trillion seconds

Russia diversifies into Canadian dollars

Russia’s

central bank announced on Wednesday that it had started buying Canadian dollars and securities in a bid to diversify its foreign

exchange reserves.

Analysts

said the move could be a sign of increased diversification of emerging market central bank assets away from the dollar and

into investments denominated in other commodity-linked currencies.

The global economy will suffer the fallout from the financial

crisis for years to come, the World Bank said... in a report warning that growth may wilt later this year as stimulus spending

fades.

The Washington-based bank forecasts the world economy will

grow 2.7 percent this year, and 3.2 percent in 2011. It contracted 2.2 percent in 2009.

"A great deal of uncertainty clouds the outlook for the second

half of 2010 and beyond," the report said.

Though the "acute phase" of the crisis has passed, chronic

weaknesses remain. Much depends on the timing of withdrawal from massive stimulus programs and adjustments to monetary policy,

the bank said.

Mishandling could result in a "double-dip," with a return to

recession in 2011, it warned.

China appears to be on the brink of overtaking beleaguered Japan as the

world's second-biggest economy after another blistering performance in 2009...

Asia's two biggest economies look to have ended 2009 in a tight race but

China, which grew 8.7 percent last year, is soon expected to unseat its neighbour from the position it has held for more than

40 years...

China...reported nominal -- unadjusted for inflation -- gross domestic

product (GDP) for 2009 of 33.5 trillion yuan, or 4.9 trillion US dollars at today's exchange rates...

Japan posted nominal GDP of about 505.1 trillion yen, or 5.5 trillion

US dollars, in 2008 and its economy is expected to have shrunk by roughly six percent last year, reducing the figure to about

5.2 trillion US dollars...

Risk that deteriorating

government finances could push economies into full-fledged debt crises tops a list of threats facing the world in 2010.

Report by the World

Economic Forum says

high debt has become a growing concern for financial

markets. The risk is particularly high for developed nations, as many emerging economies, not least in Latin America, have

already been forced by previous shocks to put their fiscal houses in order (see below on this page for more details on the

WEF report).

Chinawill slow its massive lending spree and

step up monitoring of banks as it tries to prevent speculative bubbles in real estate and other assets while keeping the country's

economic recovery on track

Investment

expert and author Stephen Leeb believes we're entering the beginning of the end when it comes to thecommoditiesthat hold our modern

world together. Resources such as oil, copper and iron are being rapidly depleted -- and with the needs of developing countries,

demands are only increasing.

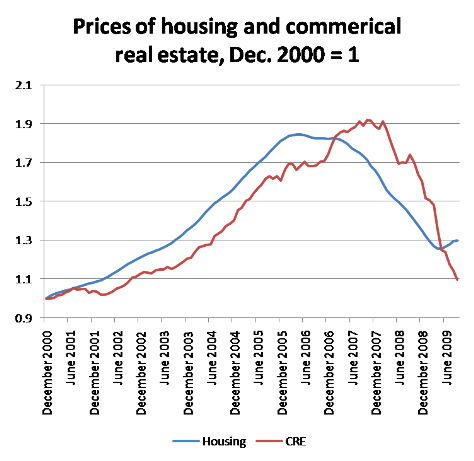

Five Potential Potholes on the Road to U.S. Recovery

1. Employment continues

to decline...2.Commercial real estate (CRE) foreclosures continue rising, more banks go belly up...3. Residential real estate's advance halts...4. China's real estate bubble

pops...5. U.S. Sales and income taxes keep declining

The U6 unemployment rate counts not only people

without work seeking full-time employment (the more familiar U-3 rate), but also counts "marginally attached workers and those

working part-time for economic reasons."Note that some of these part-time workers

counted as employed by U-3 could be working as little as an hour a week. And

the "marginally attached workers" include those who have gotten discouraged and stopped looking, but still want to work.The age considered for this calculation is 16 years and over

____________________________________________

Moody’s Investors Service

“Latin America and the Caribbean have come out of the crisis with

relatively little new debt, especially when compared to more developed parts of the world, leaving the region in a good position

at the start of 2010...For the first time in years, if not decades, a major crisis has passed without substantial increases

in the regional debt burden or a fall in international reserves.”

THIS WEEK'S REPORTS

Election Finance Reform Report

In addition to extensive new information about the role of

small and large doors in federal and state elections, the fifty-five page report contains this report offers a new vision

of how campaign finance and communications policy can help further democracy through broader participation.

"My resolve to reform the system is only strengthened when

I see a return to old practices at some of the very firms fighting reform and when I see record profits at some of the very

firms claiming that they cannot lend more to small business, cannot keep credit card rates low, and cannot refund taxpayers

for the bailout"

___________________________________

Stephen Dinan, Washington Times

"In a decision with profound implications for the role of money in American

campaigns, the Supreme Court on Thursday gave interest groups, unions and corporations the right to pour money into issue

advertising in political races - reigniting the passionate battle over the influence of cash on the electoral process."

“The announcement of an agreement to create a presidentially

appointed fiscal commission that will report to the Congress and be assured a vote on its recommendations is a major step

toward putting our nation’s financial house in order while protecting our social safety net programs.”

_________________________________________

Columbia University

professor and Nobel Laureate, Joseph Stiglitz:

U.S. does not have capitalism..."In old-style 19th Century capitalism, I owned my company, I made

a mistake, Ibore the consequences. Today, (at) most of the big companies you have managers who, when things go well,

walkoff with a lot of money. When things go badtheshareholders bear the costs."...the American systemnow socializes the losses and “privatizesthe gains.”

Premio

Nobel y profesor de la Universidad de Columbia Joseph Stiglitz:

"En EEUU ya no hay

capitalismo...

Una horrible cantidad de gente no está gestionando su propio dinero.

En el viejo capitalismo del Siglo XIX, yo poseía mi empresa y, si cometía un error, sufría las consecuencias. Hoy, en la mayoría

de las grandes empresas, tienes gestores que, cuando las cosas van bien, se llevan muchísimo dinero, y cuando van mal, los

accionistas corren con los costes...Es un sistema en elque se socializan las pérdidas y se privatizan

las ganancias."

_________________________________________

Director general del FMI, Dominique

Strauss-Kahn

"Necesitamos

reformas y una voluntad política...Mi preocupación es que en seis o doce meses todo el mundo retome su actividad como antes

y se olviden las lecciones de la crisis financiera".

___________________________________

Justin Lin, World Bank chief economist

"Unfortunately,

we cannot expect an overnight recovery from this deep and painful crisis, because it will take many years for economies and

jobs to be rebuilt. The toll on the poor will be very real"

THIS WEEK'S POLLS

.

.

.

DR.DOOM SAYS...

"...monetization of...fiscal deficits is becoming a pattern in many advanced economies,

as central banks have started to swell the monetary base via massive purchases of short-and long-term government paper. Eventually,

large monetized fiscal deficits will lead to a fiscal train wreck and/or a rise in inflation expectations that could sharply

increase long-term government bond yields and crowd out a tentative recovery...Fiscal

stimulus is a tricky business...If they remove the stimulus

too soon by raising taxes, cutting spending and mopping up the excess liquidity, the economy may fall back into recession

and deflation. But if monetized fiscal deficits are allowed to run, the increase in long-term yields will put a chokehold

on growth....Americans are deluding themselves that

they can enjoy European-style social spending while maintaining low tax rates....

Monetizing the fiscal deficits...(is)...the

path of least resistance: Running the printing presses is much easier than politically painful deficit reduction.

But if the U.S. does use the

inflation tax as a way to reduce the real value of its public debt, the risk of a disorderly collapse of the U.S. dollar would

rise significantly....A disorderly rush to

the exit could lead to a dollar collapse, a spike in long-term interest rates and a severe double-dip recession.

Will America be the next great

power to fall because of unsound finance?

The question is particularly

pressing in the midst of what is widely seen as the worst financial crisis since the

Great Depression...the

United States may be succumbing to financial overstretch. Deeply in debt to the rest of the world, it has become part of a

“dual country” --- “Chimerica.” “In effect, the People’s

Republic of China has become banker to the United States of America.”... Until the current global financial crisis,

this seemed to be a fairly reliable relationship. American consumers over-bought goods and over-borrowed from China, and the

Chinese in turn accumulated huge dollar surpluses that they plowed back into Wall Street investments, thereby supplying profligate

Americans with the financing we needed to consume and sustain ourselves as the lone superpower. “For a time it seemed

like a marriage made in heaven,”... “The East Chimericans did the saving. The

West Chimericans did the spending..”

Suddenly, however, it’s looking more

like a marriage made in hell...much of the current crisis stems from this increasingly uneasy symbiosis. It turns out “there

was a catch. The more China was willing to lend to the United States, the more Americans were willing to borrow.” This

cascade of easy money...“was the underlying cause of the surge in bank lending, bond issuance and new derivative contracts

that Planet Finance witnessed after 2000. . . . And Chimerica — or the Asian ‘savings

glut,’ as Ben Bernankecalled it — was the underlying reason why the U.S. mortgage

market was so awash with cash in 2006 that you could get a 100 percent mortgage with no income, no job or assets.” Going

forward, the system seems likely to be increasingly unstable, as Treasury Secretary Henry Paulson suggested recently when

he warned that unless fundamental changes are made, “the pressure from global imbalances will simply build up again

until it finds another outlet.”

Previous periods of global stability and peace had relied

on

Extract from book review by Michael Hirsch of...

THE ASCENT OF MONEY

A Financial History of the World

By Niall Ferguson

Illustrated. 442 pp. The Penguin Press. $29.95 Published

November 13, 2008

judicious mechanisms like the Congress of Vienna or the Bretton Woods agreements. Now the international system —

and America’s position within it — has come to depend on what looks more like a global Rube Goldberg machine running

on hot money...the Chinese may now have the upper hand in this chimerical Chimerica. While

so far it’s worked in Beijing’s interest to under write America’s rampant consumerism — because we

buy so many of their goods — the Chinese also have the option of recycling some of their surplus billions into their

own huge population. We, on the other hand, don’t have the option not to borrow from them. Indeed, it’s no secret

on Wall Street and in Washington that the real targets of President Bush’s $700 billion bailout plan were the foreign

funds, including “

sovereign wealth funds,” that keep America’s financial system afloat.

Unless these foreign financiers — principally China and Japan — get reassurance that the global financial system

can function properly again, America’s long period of growth and power may be coming to a close. Perhaps, then, the conclusion should be that Americans

need to flex our muscles less as an empire and fight a little harder for fiscal sobriety and balance in our foreign policy.

Without doubt, the United States is exhibiting some of the classic precursors to out-of-control

inflation. But a deeper look suggests that the story is not so simple...

One basic lesson of economics is that prices rise when the government creates an excessive

amount of money. In other words, inflation occurs when too much money is chasing too few goods.

A second lesson is that governments resort to rapid monetary growth because they face

fiscal problems. When government spending exceeds tax collection, policy makers sometimes turn to their central banks, which

essentially print money to cover the budget shortfall.

Those two lessons go a long way toward explaining history’s hyperinflations, like

those experienced by Germany in the 1920s or by Zimbabwe recently. Is the United States about to go down this route?

Recession:As

federal spending and debt soar to new highs, many economists have alarmingly concluded that the dollar will soon collapse

and take the economy with it. But that scenario is far from inevitable.

You don't have to look far to see the red flags flapping. Most recently,

the respected 24-member Committee On the Fiscal Future of the United States warned the U.S. must cut its debt or face a dollar

crisis.

"It has got to be done," said Rudolph Penner, formerly head of the

nonpartisan Congressional Budget Office and the group's co-chair. "It will be done some day. It may be done with enormous

pain. Or it may be done more rationally."

In the same vein, commentator Patrick Buchanan wondered in his latest

column, "Is America's Financial Collapse Coming?" And these concerns are far from isolated. A Google search of "dollar" and

"crisis" yielded 57.5 million hits.

We too have said the government's massive spending and debt pose real

dangers. Average federal spending from World War II through 2008 was about 20% of gross domestic product. Today, it's 26%

— and climbing. Worse, just one year ago total U.S. public debt was $5.8 trillion. Today it's $12 trillion, and rising

literally by the minute.

Even so, we believe a full-blown dollar crisis — involving a

collapse in our currency and an inability to pay our debts — is unlikely.

• Over two-thirds

of people believe the current economic crisis is also a crisis of ethics and values • Report based on opinion

poll of over 130,000 respondents from 10 G20 economies on Facebook • Global religious leaders identify the key

values for a more just and sustainable post-crisis economy

Over two-thirds of people believe the current

economic crisis is also a crisis of ethics and values. But only 50% think universal values exist. These are among the findings

of the World Economic Forum’s Faith and the Global Agenda: Values for the Post-Crisis Economy, an annual report on issues

related to the role of faith in global affairs.

Almost two-thirds of respondents believe that people do not

apply the same values in their professional lives as they do in their private lives

When

asked to identify the values most important for the global political and economic system, almost 40% chose honesty, integrity

and transparency

“The

economic and financial crisis is an opportunity to re-articulate the values that should underpin our global institutions going

forward,” said John J. DeGioia, President of Georgetown University, USA. “The world's religious communities are

critical repositories of those values.

The social sins that Mahatma Gandhi used to instruct his young disciples in his ashram are:

"...there are

those which feature highly on the Global Risks Landscape and which predated the recession

but have been exacerbated by its impact through greater

resources constraints or short-term thinking.

These include:

Fiscal crises and the social and political implications of high unemployment

Underinvestment in infrastructure,

both new and existing, and its consequences for growth, resource scarcity and climate change adaptation

Chronic diseases and their impact on both advanced economies and developing countries

The report also notes how concerns over further asset

bubbles remain strong...

The other risks discussed in this report are equally

systemic in nature and also require better global governance but they currently feature less prominently on the Global Risks

Landscape. The report raises these risks to understand if there is an “awareness gap” around these areas and suggests

that they should not be forgotten in the focus on an integrated and longer term view of risks. These risks include:

transnational crime and corruption;

biodiversity loss; and

cyber-vulnerability."

Economic Risks

Food price volatility - Rising and volatile prices affect poor

consumers globally (those whose consumption basket is more than 50% food)

Oil price spikes - Sharp and/or sustained

oil price increases place further economic pressures on highly oildependent industries and consumers, as well as raising geopolitical

tensions

Major fall in the US dollar - An abrupt, major fall

in the value of the US dollar with impact throughout the global economic and financial systeM

Slowing Chinese economy - Sudden reduction in China’s growth to 6% or less

Fiscal crises - Overstretch of fiscal positions generates unsustainable levels of debt, rising interest rates, inflationary pressures

and sovereign debt crises

Asset price collapse - A collapse of real and

financial assets in advanced and emerging market economies leads to the destruction of wealth, deleveraging, reduced household

spending and demand

Retrenchment from globalization (developed) - Multiple developed economies

adopt policies that create barriers to flows of goods, capital and labour and fail to engage with multilateral governance

structures to address global challenges

Retrenchment from globalization (emerging) - Multiple emerging economies

adopt policies that create barriers to flows of goods, capital and labour and fail to engage with multilateral governance

structures to address global challenges

Burden of regulation - If not balanced, regulation can have

unintended consequences for Industry structures and market competition, distorting the allocation of capital and constraining

investment and the power to innovate

Underinvestment in infrastructure - Failure to invest in

physical or intangible infrastructure hinders growth and development and results in major loss of resilience

Geopolitical Risks - International terrorism, Nuclear

proliferation, Iran, North Korea, Afghanistan

instability, Transnational crime and corruption, Israel-Palestine,

Iraq, Global

governance gaps

Environmental Risks - Extreme weather, Droughts and desertification, Water scarcity, National Catastrofe - Cyclone, Earthquake, Inland

flooding, Coastal flooding, Air pollution, Biodiversity loss

Societal Risks - Pandemics, Infectious diseases, Chronic diseases, spread of US-style liability regimes to other jurisdictions, Migration

Technological Risks - Cyberspace attacks

or system failures, Nanoparticle toxicity, Data fraud/loss

"Leaders now recognize that the world is inadequately equipped to deal with global risks. The context in which

decisionmaking processes happen has shifted radically from one where the immediate prevailed to one where a long-term perspective

is vital. To fight systemic crises effectively we need systemic risk management. This report is a reminder of the urgency

for action at individual, corporate, national and supra-national levels. “Going back to business as usual” is

no longer an option. Behaviour needs to change at all levels: individual, corporate, political, if new, more forwardlooking

models and mechanisms for global governance are to be truly effective in managing the risks the world faces.

(Webmaster comment: I believe this is worth reading and considering. - JW)

Post-Crisis Reforms: Some

Points to Ponder

by MUHAMMAD TAQI USMANI

,

Vice President, Darul-Uloom Karachi

The following is an extract from a paper by Justice Muhammad

Taqi Usmani is an eminent Hanafi Islamic scholar from Pakistan included in the World Economic Forum report "Values for the

Post-Crisis Economy" cited above:

A glance over the present

crisis

Let us now have a glimpse of how the present crisis emerged to find out its root causes in the

light of the principles highlighted above. Until early 2007, there was a boom in US household credit. Financial institutions

raced towards offering house loans at competitive rates of interest. In order to refinance these loans, they were sold to

factoring agencies that securitized them for the general public. Risky loans were packaged in “collateralized debt obligations”

(CDOs) with a claim that pooling these debt obligations according to a mathematical magic erodes their risk to a great extent.

Agencies, therefore, rated them as AAA.These CDOs were then sliced up and exported throughout the

world. This prompted Wall Street to create new CDOs of low-rated corporate bonds. Once CDOs exhausted the available debts,

derivatives in the form of credit default swaps (CDS) came into the picture. By 2008, the credit default swaps market had

grown to US$60 trillion, while the entire world’s GDP was US$60 trillion. During the same time, the size of the derivatives

markets overall had increased to an incredible US$600 trillion—most of this money was unregulated.

When house prices dropped, the obligors of house loans defaulted. Foreclosures were insufficient

to recover the dues. It transpired that these debt-based assets were not safe.This created a panic, and the whole pyramid

of debt-based instruments fell down. Once panic set in, lending was stopped, companies suffered losses, and share prices faced

steep falls.The whole economic setup was in the grip of the crisis that is estimated to have wiped out nearly 45% of the wealth

of the world.

Causes and remedies

This review shows that there were four basic factors responsible for the crisis:

1. Diverting “money” from its basic function as a medium of exchange, and making itself an object

of trade that turned the whole economy into a balloon of debts over debts.

Even in the Depression of 1930s, the Economic Crisis Committee formed by the Southampton Chamber of Commerce,

after discussing the basic causes of the problem, observed that:

In order to ensure that money performs its true

function of operating as a means of exchange and distribution, it is desirable that it should cease to be traded as a commodity.

In order to save the world from such evil consequences, this recommendation must be adhered to.

An exchange of different currencies is, of course, inevitable for the purpose of international trade. So far

as these exchange transactions are carried out for the genuine purpose of cross-border trade, they cannot pose a problem.

The problem is caused by speculative transactions in money itself. At present, the majority of

currency transactions in the market are purely speculative.The volume of global international trade in 2008 was

approximately US$32 trillion, making an average of US$88 billion on a daily

basis; the daily turnover in global foreign exchange markets is estimated at US$3.98 trillion, 9 that is, 45 times more than the volume

of international trade. It means that only 2% of trade in currencies is based on the genuine cross-border trade, while 98%

of currencies transactions account for nothing but speculation in money prices.This artificial use of currencies is the main

cause of the perpetual fluctuations in their prices that has almost stopped the function of money as a store of value.

Moreover, one of the essential requirements for restricting money to its basic function is that

interest should be abolished from financing activities. Serious thought must be given to reshaping our financial system on

the basis of equitable participation in productive activities to minimize debt transactions, which must be backed by real

assets and created only by real trade transactions of sale or lease and so on.

2. Derivatives were one of the basic causes of the financial problems. Frank Partony, a former

derivatives trader, observes:

The mania, panic and crash had many causes. But if you are looking for a single word to use in

laying blame for the recent financial catastrophe, there is only one choice: Derivatives.

The worth of total derivatives was nearly US$741.1 trillion (741,100,000,000,000) in 2008,

11 while the total

GDP of the entire world was only 60.6 trillion—that is, the worth of derivatives was 12 times more than the gross products

of all the countries of the globe.

In order to curb this evil, derivatives must be banned.

3. Sale of debts was one of the most prominent causes of this crisis. Packaging a large amount

of debt in a bundle of CDOs, which was the initial cause of the present crisis, would not be possible if sale of debts was

disallowed.

Since a genuine sale is meant to transfer the sold item to the buyer, it is logical that the seller

should have full control of the sold item to be able to deliver it to the buyer.The same principle is applicable to debts.

Since it is not absolutely certain that the obligors will fulfill their obligations, the creditor should not be allowed to

sell these debts to anyone, thereby transferring the risk of default to the buyer.This is one of the reasons why the sale

of debts is prohibited in Islamic jurisprudence.

4. Short sales in stocks, commodities and currencies is the basic factor that makes speculation

an obstacle in the smooth operation of real commercial activities. Realizing the bad effects of short selling, many regulatory

authorities resorted to a temporary ban on shorting.

In order

to avoid the lethal consequences of speculation, short sales should not be allowed any more.

To sum up: we are in the burning need of a visible change in our economic set-up on the basis of the principles

mentioned above.

To quote

the remarks of the chairman of the World Economic Forum in its last annual meeting:

Today we have reached a tipping point, which leaves us only one choice—change or face continued

decline and misery.

(From a footnote to the above paper: G. William

Domhoff has summarized this concentration in the United States in the following words: “In the United States wealth

is highly concentrated in a relatively few hands. As of 2007, the top 1% of households (the upper class) owned 34.6% of all

privately held wealth, and the next 19% (the managerial, professional and small business stratum) had 50.5%, which means that

just 20% of the people owned a remarkable 85%, leaving only 15% of the wealth for the bottom 80% (wage and salary workers).

In terms of financial wealth (total net worth minus the value of one’s home), the top 1% of households had an even greater

share: 42.7%.”)

McKinsey Global Institute Report

"...few things matter more for the world economy than

whether, and how fast, the rich world’s borrowing is cut back. History suggests that severe financial crises are usually

followed by long periods of debt reduction—in which credit falls relative to the size of the economy."

The recent bursting of the great global credit bubble

not only led to the first worldwide recession since the 1930s but also left an enormous burden of debt that now weighs on

the prospects for recovery. Today, government and business leaders are facing the twin questions of how to prevent similar

crises in the future and how to guide their economies through the looming and lengthy process of debt reduction, or deleveraging.

To help address these questions, the McKinsey Global

Institute launched a research effort to understand the growth of debt and leverage before the crisis in different countries,

the economic consequences of deleveraging, and the practical implications for policy makers, financial regulators, and business

executives. In the course of the research, MGI created an extensive fact base on debt and leverage in each sector of ten mature

economies and four emerging economies. In addition, MGI analyzed 45 historic episodes of deleveraging, in which an economy

significantly reduced its total debt-to-GDP ratio, that have occurred since 1930.

This analysis adds new details to the picture of how

leverage grew around the world before the crisis and how the process of reducing it could unfold. MGI finds that:

Leverage levels are still very high in some sectors

of several countries—and this is a global problem, not just a U.S. one.

To assess the sustainability of leverage, one must

take a granular view using multiple sector-specific metrics. The analysis has identified ten sectors within five economies

that have a high likelihood of deleveraging.

Empirically, a long period of deleveraging nearly always

follows a major financial crisis.

Deleveraging episodes are painful, lasting six to seven

years on average and reducing the ratio of debt to GDP by 25 percent. GDP typically contracts during the first several years

and then recovers.

If history is a guide, many years of debt reduction

are expected in specific sectors of some of the world’s largest economies, and this process will exert a significant

drag on GDP growth.

The right tools could have identified the unsustainable

build-up of leverage in pockets of several economies in the years leading up to the crisis. Policy makers should work to develop

a more robust system for tracking leverage at a granular level across countries and over time. One needs to look at specific

metrics such as the growth of leverage, and the borrowers' ability to service debt if there is a disruption to income or rise

in interest rates. MGI found that sufficiently granular data do not exist today.

MGI's analysis provides support for several of the

current regulatory proposals, including improving the quality of bank capital through higher Core Tier I ratios, monitoring

leverage as a proxy for asset bubbles, and creating better macro-prudential regulation to reduce systemic risk. However, the

analysis raises questions about some aspects of the current regulatory agenda, such as limiting gross leverage ratios (which

did not change appreciably in most banks).

Coping with pockets of deleveraging is also a challenge

for business executives. The process portends a prolonged period in which credit is less available and more costly, altering

the viability of some of business models and changing the attractiveness of different types of investments. In historic episodes,

private investment was often quite low for the duration of deleveraging. Today, the household sectors of several countries

have a high likelihood of deleveraging. If this happens, consumption growth will likely be slower than the precrisis trend,

and spending patterns will shift. Consumer-facing businesses have already seen a shift in spending toward value-oriented goods

and away from luxury goods, and this new pattern may persist while households repair their balance sheets. Business leaders

will need flexibility to respond to such shifts.

Summary of Commentary on Current Economic Conditions by Federal Reserve

District

Commonly known as the Beige Book,this report is published eight times per year

Reports from the twelve Federal Reserve Districts indicated that while economic activity remains at a low level,

conditions have improved modestly further, and those improvements are broader geographically than in the last report. Ten

Districts reported some increased activity or improvement in conditions, while the remaining two--Philadelphia and Richmond--reported

mixed conditions. The last Beige Book reported eight Districts with increased activity or improving conditions and four Districts

showing little change and/or mixed conditions...

...Consumer spending in the recent 2009 holiday season was modestly greater

than in 2008 for eight Districts......

...Auto sales were flat or up slightly for some dealers...

...Districts reporting on

nonfinancial services generally indicated an upward trend in activity, although in some areas reports were mixed...

...Manufacturing activity

has improved since the last report in six Districts...

...Homes

sales increased toward the end of 2009 in most Federal Reserve District...

...Nonresidential

real estate conditions remained soft in nearly all Districts...

...Loan

demand continued to decline or remained weak in most Districts...

...A number of Districts reported that credit quality continued to deteriorate. Financial

institutions in the New York District reported ongoing increases in delinquencies for all types of loans....

...Federal Reserve District Banks reporting on agricultural conditions generally indicated that cold weather at the turn of the year had adversely affected crops and stressed

livestock...

...Production of energy-related

materials has risen moderately...

...Labor market conditions

remained soft in most Federal Reserve Districts, although New York reported a modest pickup in hiring...

...Pricepressures remained

subdued in nearly all Federal Reserve Districts, although increases in metals prices were noted

in Boston, Cleveland, Minneapolis, Dallas, and San Francisco. Raw materials prices, other than metals, were reported to be

mostly steady...

...Most Districts reported

that retail prices have been steady....

prices

start to spiral into the stratosphere once the deficits as a share of government expenditure rises above a third and stays

there for several years.

InWinnie-the-Pooh, there is a significant moment when the bear is asked whether

he wants honey or condensed milk with his bread. He replies “both”. You can get away with this sort of thing if

you are a much loved character in children’s literature. But it is more problematic when great nations start behaving

in a childish fashion. When Americans are asked what they want – lower taxes, more lavish social spending or the world’s

best-funded military machine – their collective answer tends to be “all of the above”.

The result is that the US is piling up debt. A budgetdeficitof

about 12 per cent of gross domestic product is understandable as a short-term reaction to a huge financial crisis. What should

worry Americans is that, with entitlement spending set to surge, there is no credible plan to bring the budget deficit under

control over the medium term.

The

US has formidable strengths that will allow its government to be profligate for far longer than other nations could get away

with. But if the US keeps running huge deficits, sooner or later the country will start flirting with bankruptcy. Oddly, it

might be best if the crisis came sooner rather than later. For a surprising number of countries, running out of money has

been the prelude to national renewal.

The

two biggest and most beneficial geopolitical stories of the past 30 years – the spread of democracy and of globalisation

– were driven by a succession of states finding their coffers empty.

Focus on Beating Inflation and on Genuinely Productive Enterprise

...too much of the GDP is really just the velocity of

money and not real production, and there are too many jobs in the U.S. that are not productive work.

Nearly

$5 trillion of the total U.S. GDP of $14 trillion is legal fees, consultants' fees, and payments to financial-transaction

facilitators, reflecting the overlawyered nature of the country and the excessive preoccupation with deal-making (with insufficient

attention to whether the deals are wise or not). Medical activities consume another $2.5 trillion, at least $1 trillion of

that traceable to the fact that the recipient of coverage is usually not the person who pays for it, and the fact that the

legal-preventive component is excessive...

U.S. Chamber warns of 'double-dip' recession because of Dem policies

U.S. Chamber of Commerce President Tom Donohue warned

the U.S. faces a double-dip recession because of the taxes and regulations under consideration by the Democratic Congress

and President Barack Obama.

“Congress, the administration and states must recognize that our weak economy simply

could not sustain all the new taxes, regulations and mandates now under consideration. It’s a sure-fire recipe for a

double-dip recession, or worse,” Donohue said in a speech providing the Chamber's outlook for 2010.

America slides deeper into depression as Wall Street revels

December was the worst month for US unemployment since the Great

Recession began

History

repeating itself? President Obama has been accused by some economists of making the same mistakes policymakers in the US made

in the Great Depression, which followed the Wall Street crash of 1929, picturedPhoto: AP

The labour force

contracted by 661,000. This did not show up in the headline jobless rate because so many Americans dropped out of the system.

The broad U6 category of unemployment rose to 17.3pc. That is the one that matters.

Wall Street rallied.

Bulls hope that weak jobs data will postpone monetary tightening: a silver lining in every catastrophe, or perhaps a further

exhibit of market infantilism.

The home foreclosure

guillotine usually drops a year or so after people lose their job, and exhaust their savings. The local sheriff will escort

them out of the door, often with some sympathy –– just like the police in 1932, mostly Irish Catholics who tithed

1pc of their pay for soup kitchens.

Realtytrac says defaults

and repossessions have been running at over 300,000 a month since February. One million American families lost their homes

in the fourth quarter. Moody's Economy.com expects another 2.4m homes to go this year. Taken together, this looks awfully

like Steinbeck'sGrapes of Wrath.

Judges are finding

ways to block evictions. One magistrate in Minnesota halted a case calling the creditor "harsh, repugnant, shocking and repulsive".

We are not far from a de facto moratorium in some areas.

This is how it ended

between 1932 and 1934, when half the US states declared moratoria or "Farm Holidays". Such flexibility innoculated America's

democracy against the appeal of Red Unions and Coughlin Fascists. The home siezures are occurring despite frantic efforts

by the Obama administration to delay the process.

It

takes heroic naivety to think the US housing market has turned the corner ... The fuse has yet to detonate on the next

mortgage bomb, $134bn (£83bn) of "option ARM" contracts due to reset violently upwards this year and next...

The Fed's own Monetary Multiplier crashed to an all-time low of 0.809 in mid-December.

Commercial paper has shrunk by $280bn ($175bn) in since October. Bank credit has been racing down a hair-raising black run

since June. It has dropped from $10.844 trillion to $9.013 trillion since November 25. The MZM money supply is contracting

at a 3pc annual rate. Broad M3 money is contracting at over 5pc...

China becomes biggest exporter, edging out Germany

Already the biggest auto market and steel maker, China edged past Germany

in 2009 to become the top exporter, yet another sign of its rapid rise and the spread of economic power from West to East.

Total 2009 exports were more than $1.2 trillion, China's customs agency

said Sunday. That was ahead of the 816 billion euros ($1.17 trillion) forecast for Germany by its foreign trade organization,

BGA.

China's new status is mostly symbolic but highlights its growing presence

as an industrial power, major buyer of oil, iron ore and other commodities and, increasingly, as an investor and key voice

in managing the global economy.

China supplanted the U.S. as the world’s

largest auto market after its 2009 vehicle sales jumped 46 percent, ending more than a century of American dominance that

started with theModel TFord.

The nation’s sales of passenger cars, buses and

trucks rose to 13.6 million, the fastest pace in at least 10 years, according to the China Association of Automobile Manufacturers.

In the U.S., sales slumped 21 percent to 10.4 million, the fewest since 1982, according to Autodata Corp.

China’s vehicle sales have surged since

1999 as economic growth averaging more than 9 percent a year has helped automakers includingGeneral Motors Co.andVolkswagen AGcompensate

for slumping demand in the U.S. and Europe. The market will likely remain the world’s largest, even as sales slow this

year on a reduction in tax cuts, according to Booz & Co.

“China is becoming the center stage

of development for the 21st century global auto industry,” saidBill Russo, a Beijing- based senior adviser at Booz &