The private sector

plays a pivotal role in fighting corruption worldwide. Transparency International’s Global Corruption Report 2009 documents in unique detail the many corruption risks for businesses, ranging from small entrepreneurs in

Sub-Saharan Africa to multinationals from Europe and North America. More than 75 experts examine the scale, scope and devastating

consequences of a wide range of corruption issues, including

bribery

and policy capture

corporate fraud

cartels

corruption in supply chains and transnational transactions

emerging

challenges for carbon trading markets

sovereign wealth funds and

growing economic centres, such as Brazil, China and India.

The Global Corruption Report 2009 also

discusses the most promising tools to tackle corruption in business, identifi es pressing areas for reform and outlines how

companies, governments, investors, consumers and other stakeholders can contribute to raising corporate integrity and meeting

the challenges that corruption poses to sustainable economic growth and development.

The massive scale

of global corruption resulting from bribery, price-fixing cartels and undue influence on public policy is costing billions

and obstructing the path towards sustainable economic growth, according to a new report released today by Transparency International

(TI).

The Global Corruption Report 2009: Corruption and the Private Sector (GCR) shows how corrupt practices constitute a destructive force that undermines fair competition,

stifles economic growth and ultimately undercuts a business’s own existence. In the last two years alone, companies

have had to pay billions in fines due to corrupt practices. The cost extends to low staff morale and a loss of trust among

customers as well as prospective business partners.

“Fostering

a culture of corporate integrity is essential to protect investment, increase commercial success and ensure the stability

sought by poor and rich countries alike, particularly as we climb out of an historical crisis,” said TI Chair Huguette

Labelle.

The report documents many cases of

managers, majority shareholders and other actors inside corporations who abuse their entrusted power for personal gain, to

the detriment of owners, investors, employees and society at large. In developing and transition countries alone, companies

colluding with corrupt politicians and government officials, have supplied bribes estimated at up to US $40 billion annually,

according to the GCR.

Research in the report

also shows that half of international business executives polled estimated that corruption raised project costs by at least

10 per cent. Ultimately, it is citizens who pay: consumers around the world were overcharged approximately US $300 billion

through almost 300 private international cartels discovered from 1990 to 2005.

Another concern addressed in the report is how the sheer economic power of some companies and

business sectors translates into disproportionate and undue leverage on political decision-making. Failure to regulate such

influence lays the foundation for kleptocratic systems and stunted growth. Lobbying efforts often lack transparency and tend

to fall outside the system of checks and balances that firms rely on for strategic decisions. For example, in 2008, roughly

one-third of Standard & Poor’s 100 companies required board oversight of political spending.

Revolving doors between public office and the private sector, another

practice documented in the report, provide a smooth path to deceitful public procurement deals where non-competitive bidding

and opaque processes lead to immense waste and unreliable services or goods.

The extent and multifaceted ways in which private sector corruption is manifested greatly surpasses

the few companies that actually employ systems to stop this abuse of power for illicit gain. Almost 90 per cent of the top

200 businesses worldwide have adopted business codes, but fewer than half report that they monitor compliance, according to

the report.

Many of the countries found at the

bottom of TI’s yearly Corruption Perceptions

Index – which measures perceived levels

of public-sector corruption in over 170 countries – are not only victim to unscrupulous governments but to major firms

that are more than willing to enter into corrupt deals with these governments. These intricate webs, involving more than simple

bribes, are possible because companies believe that they can get away with such criminal practices.

“Basing a company or fund’s future on personal relationships

and unpredictable systems or simply operating in a dark space without oversight and accountability is a path to guaranteed

failure,” said Labelle.

Corporate integrity

pays. Companies with anti-corruption programmes and ethical guidelines are found to suffer up to 50 per cent fewer incidents

of corruption and to be less likely to lose business opportunities than companies without such programmes. The tools for corporate

anti-corruption action are broadly and readily available but companies must pick up the pace in applying them.

The dearth of confidence in corporate ethics highlighted by the present

economic crisis makes the need to promote anti-corruption mechanisms, as an integral part of a company’s operations,

all the more urgent.

“Winning on anti-corruption

means adding to the bottom line. It is time that corporations face up to the risk of paying millions in fines and the long-term

loss of trust from their customers and shareholders,” added Labelle. Forward thinking CEOs are already acting forcefully

against corruption and reducing risks in an effort to secure sustainable business growth with integrity at the core of their

operations.

Corporate integrity is about more

than sustainable earnings or returns on investment. When reckless companies engage in corruption, the consequences can be

devastating. From water shortages, exploitative work conditions or illegal logging to unsafe medicines and poorly or illegally

constructed buildings that collapse with deadly consequences, corruption can bring about unprecedented harm. The private sector

has a crucial role to play in preventing these outcomes, by operating with transparency and accountability wherever there

is a profit to be made.

U.S. issues $7

trillion debt,

supply to

stabilize

The U.S. government will have

issued $7 trillion in bonds by the time the current fiscal year ends next week, but it expects the debt deluge to stabilize

by mid 2010, a Treasury official said on Wednesday.

Though markets and the economy are improving, efforts

to provide a firm foundation for recovery will require increases to the U.S. Treasury's conventional bonds going forward,

as well as debt securities that are indexed to inflation.

However,

this expansion may take place in an environment where investors consider leaving the safe-haven Treasury market for riskier

assets, and debt issuance is likely to level off mid next year, said Treasury Acting Assistant Secretary for Financial Markets

Karthik Ramanathan.

"In fiscal year 2009, which

ends next week, Treasury will have issued $7 trillion in gross issuance -- that's in a 12-month period," Ramanathan told a

financial markets conference in New York.

"This

issuance was necessary to meet nearly $1.7 trillion in net marketable borrowing needs, nearly $1 trillion more than what we

raised last year," he added.

DEMAND TO

WANE

The heavily-indebted U.S. government

has seen tremendous demand for Treasury debt securities this year due to a flight-to-quality into the safe haven assets.

However, Ramanathan said some of this demand would

begin to taper off and investors were likely to favor other sectors as the financial markets recovery continues.

"Rather than being discouraged by this move to more

risky assets we should actually be encouraged," he said. "It is the natural progression from the state we were in last year."

The central bank has flooded the world

with dollars to avert collapse and start a recovery. But what if the U.S.

economy doesn't reap the rewards?

Whose recovery is the Fed stimulating,

anyway?

A year after the near collapse of the financial markets, the

global economy has stabilized. Job losses have slowed and stocks have posted a sharp rally.

Yet skeptics warn that a major driver of the recovery in

stock and bond markets -- a round of unprecedented emergency money printing by the Federal Reserve --

could actually slow the healing of the real economy.

In this view, the Fed's decision to hold short-term interest

rates near zero has temporarily revived financial markets without addressing the

economy's underlying problems. The danger is that with bank lending remaining

anemic and consumer balance sheets still bloated, the low U.S. rates could end

up supporting overseas growth without fortifying domestic health.

"You end up financing everybody else's expansion but your

own," said Howard Simons, a strategist at Bianco Research in Chicago.

Critics focus on the fact that low U.S. interest rates

enable investors around the globe to borrow dollars for next to nothing and

invest them elsewhere at higher rates.

The G-20's six largest economies took a big hit during the

global recession

in the past year and a half. Challenges remain but most appear on the path to

recovery.

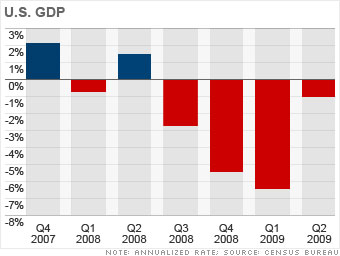

United States: Painful rebound

GDP: -1%

Inflation: -1.5%

Unemployment: 9.7%

Markets: 18.3%

Interest rate: 0% to 0.25%

The

U.S. economy appears to be stabilizing

after declining for four straight quarters, but the recovery has been tepid so

far.

Financial markets have shown signs of improvement, and interbank

lending has largely returned to normal. Consumer spending is still shrinking due

to ongoing job losses and difficult credit conditions, but it has been

stabilizing over the past quarters. Furthermore, home sales and new home

construction are beginning to make a long-awaited comeback.

Businesses

have continued to cut back on spending and have sharply reduced their

inventories. But many economists believe that companies are largely done with

their cuts, which could lay the groundwork for economic growth this quarter. The

massive $787.2 billion stimulus bill is also expected to give GDP a boost in the

current quarter.

"The recession is very likely over at this point,"

Federal Reserve Chairman Ben Bernanke said last week. But he also added, "It's

still going to feel like a very weak economy for some time."

That's

because unemployment continues to rise, retail sales are still slipping,

factories have cut output to the bare bones and wages remain depressed.

Recession-weary Americans aren't

gambling the way they used to -- and that could be a problem for many U.S.

states already struggling with record budget gaps due to the weak economy.

State revenues from all sources of authorized gambling fell

2.8% in fiscal 2009, according to a report from the Rockefeller Institute of

Government released Monday. It was the first decline in data going back at least

20 years.

"It's not a huge decline, but it's sobering," said Mark

Marchand, director of communications for the Rockefeller Institute.

Lottery income, the largest source of state gambling

revenues, fell 2.6%. It was the first annual drop in lottery revenue going back

to 1970, according to the group.

Income from casinos fell 8.5%, while revenue from

pari-mutuel wagering, which includes dog and horse racing, sank nearly 15%.

The era of U.S. economic dominance is over, pundits say, and

the future of your money is international. Take our quiz to see whether you're

really ready.

International financial crisis brings

both opportunities, challenges to China: premier

The current

international financial crisis has had a far-reaching impact on the world economy and it has brought both opportunities and

challenges to China, Chinese Premier Wen Jiabao said at a workshop here Tuesday.

Every

time a major crisis hits, it brings about new breakthroughs in science and technology, promotes an industrial revolution,

gives birth to new industries, and forms new growth points in the economy, said Wen, while presiding over a workshop on strategic

industries covering new energy, energy-efficient and environmental technologies, electricity-powered automobiles, new materials,

new medicine and pharmacy, biology and seed-breeding, and the information industry.

China

has the capabilities of taking over the commanding heights in the fields of economy and science and technology, said the premier.

El sistema financiero actual lleva

consigo el virus de la inestabilidad: AFI

La crisis mundial "aún no ha concluido"

y, peor todavía que, de cara a la próxima reunión del G-20, será imposible sentar las bases para evitar una nueva crisis financiera

internacional, advirtió Emilio Ontiveros, presidente de Analistas Financieros Internacionales (AFI).

"El sistema financiero lleva en sus entrañas un virus que transmite

inestabilidad; por tanto, evitar una futura crisis es imposible y, en este sentido, yo me conformaría con que en la reunión

del Grupo de los 20 (G-20) se sienten las bases para que la próxima crisis genere menos destrozos que los que ha originado

ésta", explicó Ontiveros en entrevista con EL FINANCIERO.

"Creo que aquí hay que asumir las posiciones de (Hyman) Minsky y otros colegas, quienes señalan que el sistema

tiene ese virus de la inestabilidad", apuntó Ontiveros, quien opinó que lo que sí podría hacer el G-20 es evitar que las crisis

se agraven cada vez más.

"Es importante

no aumentar esta tendencia maligna y perversa de que cada crisis que ha tenido lugar en los últimos 30 años ha tenido consecuencias

económicas más adversas; por ejemplo, la crisis de la deuda; luego, la de México en el 94; luego, la crisis asiática y ahora

ésta. Se ha dado una especie de espiral de crisis que lo que ha hecho es denunciar que no aprendemos; por tanto, aprendamos

por lo menos a minimizar los daños", urgió Ontiveros.

FMI hace balance positivo de las intervenciones en

la crisis y apuesta por un modelo de titulización sólida

El Fondo Monetario Internacional (FMI) hizo hoy un balance

positivo de las intervenciones estatales para combatir la crisis financiera y apostó por la elaboración de un modelo de titulización

sólida, según establece el informe de octubre sobre la estabilidad financiera global de la institución.

El Fondo, que hizo hoy públicos dos capítulos del mencionado informe, considera que "los anuncios de intervención lograron

calmar los mercados financieros en turbulencia" y que los anuncios de respaldo a la liquidez lograron un máximo de eficacia

durante las primeras fases de la crisis, en tanto que la recapitalización de los bancos y las compras de activos por parte

de las autoridades lograron un máximo de eficacia en etapas posteriores.

Según

las conclusiones de este informe, algunos instrumentos financieros ya han empezado a estabilizarse y la emisión de deuda está

repuntando "en respuesta a las medidas sin precedentes lanzadas por el sector público ante la crisis".

"La disminución del estrés en el sector bancario y el restablecimiento parcial de la autosuficiencia en los mercados son indicios

prometedores de que las intervenciones públicas más extensas en el sector financiero desde la gran depresión ayudaron a contener

el temor al riesgo sistémico", explica el Fondo, que califica de "rápidas" la respuestas de los gobiernos a la crisis.

Sobre las estrategias de salida de las medidas extraordinarias acometidas para combatir la crisis, el Fondo dice que deben

guiarse "por la reanudación de una confianza duradera en la salud de las instituciones y los mercados financieros", y establece

que no hay un modelo general del cómo ni el cuándo articularlas, debido a las variaciones de las condiciones económicas y

financieras en los distintos países.

Asia encabezará la recuperación de la crisis financiera global, dice el BAD

- Las economías de Asia, con

la china al frente, dan señales de que encabezarán la recuperación de la crisis financiera mundial, según al Banco Asiático

de Desarrollo (BAD), que hoy revisó alza la previsión del crecimiento económico de la región.

El banco multilateral

indicó que en conjunto la economía de Asia, excluida la muy avanzada de Japón, crecerá en 2009 un 3,9 por ciento, por encima

del 3,4 por ciento estimado en su previsión del pasado marzo.

También en su informe semestral, la entidad

financiera con sede en Manila, elevó desde el 6,0 al 6,4 por ciento, la previsión de crecimiento de la región en 2010.

En

relación a China, el BAD señaló que la tercera mayor economía del mundo registrará este año una expansión del 8,2 por ciento,

frente a la 7,0 por ciento prevista hace seis meses.

La de India, la otra economía emergente con mayor

peso en la región, lleva trazas de crecer el 6 por ciento en 2009, un punto porcentual superior al total estimado en principio

por el BAD.

El banco estima que en 2010, la economía de China se expandirá un 8,9 por ciento, mientras

que la de la India lo hará un 7,0 por ciento.

. LAFFER >>> The

U.S. in the early 1930s was on a gold standard where paper currency was legally convertible into gold. Both circulated in

the economy as money. At the outset of the Great Depression people distrusted banks but trusted paper currency and gold. They

withdrew deposits from banks, which because of a fractional reserve system caused a drop in the money supply in spite of a

rising monetary base. The Fed really had little power to control either bank reserves or interest rates.

The increase in the demand for paper

currency and gold not only had a quantity effect on the money supply but it also put upward pressure on the price of gold,

which meant that dollar prices of all goods and services had to fall for the relative price of gold to rise. The deflation

of the early 1930s was not caused by tight money. It was the result of panic purchases of fixed-dollar priced gold. From the

end of 1929 until early 1933 the Consumer Price Index fell by 27%.

By mid-1932 there were public fears

of a change in the gold-dollar relationship. In their classic text, "A Monetary History of the United States," economists

Milton Friedman and Anna Schwartz wrote, "Fears of devaluation were widespread and the public's preference for gold was unmistakable."

Panic ensued and there was a rush to buy gold.

In early 1933, the federal government

(not the Federal Reserve) declared a bank holiday prohibiting banks from paying out gold or dealing in foreign exchange. An

executive order made it illegal for anyone to "hoard" gold and forced everyone to turn in their gold and gold certificates

to the government at an exchange value of $20.67 per ounce of gold in return for paper currency and bank deposits. All gold

clauses in contracts private and public were declared null and void and by the end of January 1934 the price of gold, most

of which had been confiscated by the government, was raised to $35 per ounce. In other words, in less than one

year the government confiscated as much gold as it could at $20.67 an ounce and then devalued the dollar in terms of gold

by almost 60%. That's one helluva tax.

The 1933-34 devaluation of the dollar

caused the money supply to grow by over 60% from April 1933 to March 1937, and over that same period the monetary base grew

by over 35% and adjusted reserves grew by about 100%. Monetary policy was about as easy as it could get. The consumer price

index from early 1933 through mid-1937 rose by about 15% in spite of double-digit unemployment. And that's the story.

The lessons here are pretty straightforward.

Inflation can and did occur during a depression, and that inflation was strictly a monetary phenomenon.

My hope is that the people who are

running our economy do look to the Great Depression as an object lesson. My fear is that they will misinterpret the evidence

and attribute high unemployment and the initial decline in prices to tight money, while increasing taxes to combat budget

deficits.

The

United States will urge world leaders this week to launch a new push in

November to rebalance the world economy, but there are doubts national

governments will bow to external advice.

A document outlining the U.S. position ahead of the September 24-25 Group of 20 summit in

Pittsburgh said exporters, which include China, Germany and Japan, should

consume more, while debtors like the United States ought to boost

savings.

"The world will face anemic growth if adjustments in one part of the global

economy are not matched by offsetting adjustments in other parts," said the

document, which was obtained by Reuters on Monday.

The framework drafted by U.S. policy makers foresaw analysis of G20 members' economic

policies by the International Monetary Fund to figure out if they were

consistent with better balanced growth.

"We call on our finance ministers to launch the new framework by November,"

the document said, signaling a determined effort to maintain momentum for change

created by last year's global financial crisis.

The United States envisages the IMF playing a central role in a process of

"mutual assessment" by making policy recommendations to the G20 every six months.

It is a snapshot of the fragile foundations of the American economy and

the epic boulder it now finds itself trapped beneath. The graph shows total debt outstanding in the United States, both secured

and unsecured, as a percentage of GDP. In 1981 it was a manageable 168 percent, in 1996 253 percent, and by the first quarter

of 2009 with the collapse of the housing and credit bubbles it had reached a staggering 373 percent of GDP.

Given

that consumption makes up over 70 percent of the U.S. economy, the most worrying part of this huge debt burden is that of

the household sector. In 1981, household debt as a percentage of GDP was 48 percent, in 1996 66 percent, and by 2009

it was nearly 97 percent. The last time the household debt to GDP ratio was near 1:1 was 1929. The average household

credit card debt is $8,329. Undergraduates leave college with, on average, $27,803 in debt. One in four households is

"underwater" on their mortgages, meaning they have negative equity...

t is not just American households that are in trouble.

Corporate debt, particularly financial sector debt, has ballooned over the past several decades. In 1981, financial

sector debt was just 22 percent of GDP; in 1996, it had climbed to 61 percent, and then exploded during the bubbles years

to reach 120 percent of GDP in 2009...

As the private sector

painfully de-leverages, and households dramatically cut back on consumption and attempt to pay down some of their debt, the

federal government has (rightly) stepped into the breach. The $787 billion American Recovery and Reinvestment Act passed earlier

this year, while almost certainly too small, is essentially debt-financed, as will be a significant portion of this year's

budget. OMB projects the federal government debt-to-gdp ratio will this year reach 55.7 percent, its highest level since 1955....

The surest way to avoid such a fate is to jettison a central, indeed the central

axiom of post-1970s neoliberal global capitalism, and that is to embrace a period of moderate, sustained inflation.

A broad survey of Americans has provided striking measures

of the recession's

effect on life at home and at work: People are now stuck in traffic longer, less

apt to move away and more inclined to put off marriage and buying a house.

The U.S. census data, released Monday, also show a dip in the number of

foreign-born last year, to under 38 million after it reached an all-time high in

2007. This was due to declines in low-skilled workers from Mexico searching for

jobs in Arizona, Florida and California.

Health coverage swung widely by region, based partly on levels of

unemployment. Massachusetts, with its universal coverage law, had fewer than 1

in 20 uninsured residents -- the lowest in the nation. Texas had the highest

share, at 1 in 4, largely because of illegal immigrants excluded from

government-sponsored and employer-provided plans.

Demographers said the latest figures were significant in highlighting how

profoundly the recession affected Americans as it hit home in 2008. Findings

come from the annual American Community Survey, a sweeping look at life built on

information from 3 million households.

Preliminary data earlier this year found that many Americans were not moving,

staying put in big cities rather than migrating to the Sunbelt because of frozen

lines of credit. Mobility is at a 60-year low, upending population trends ahead

of the 2010 census that will be used to apportion House seats.

''The recession has affected everybody in one way or another as families use

lots of different strategies to cope with a new economic reality,'' said Mark

Mather, associate vice president of the nonprofit Population Reference Bureau.

''Job loss -- or the potential for job loss -- also leads to feelings of

economic insecurity and can create social tension.''

''It's just the tip of the iceberg,'' he said, noting that unemployment is

still rising.

U.S. leading index at 1-1/2-year high, loan defaults up

A measure of the U.S.

economy's prospects scaled a 1-1/2-year high in August but

a record rise in home loan defaults cast doubts on the durability of the

apparent recovery from recession.

The Conference Board said on Monday its index of leading economic indicators

rose 0.6 percent to 102.5, the highest level since January 2008. It had advanced

0.9 percent in July.

It was the fifth straight month that the gauge, which is supposed to forecast

economic trends six to nine months ahead, had increased. The gain was a touch

below the 0.7 percent rise economists had forecast. The index has risen 4.4

percent during the past six months.

"These data add further evidence to the growing view and our long-held belief

that the official end date of the recession is likely to be sometime in the

third quarter," said Michelle Girard, an economist at RBS in Greenwich,

Connecticut.

However, separate monthly data from credit bureau Equifax Inc showed a record 7.58 percent of U.S.

homeowners with mortgages were at least 30

days late on payments in August, up from 7.32 percent in July.

Obama Says Financial Regulations Must Be

Strengthened Globally

The President said tougher financial regulations are needed

worldwide to protect consumers, provide economic stability and prevent future

crises.

With the leaders from the Group of 20 nations set to meet next week in

Pittsburgh, Obama said in his weekly address that international cooperation has “stopped our

economic freefall.”

“We know we still have a lot to do, in conjunction with nations around the

world, to strengthen the rules governing financial markets and ensure that we

never again find ourselves in the precarious situation we found ourselves in

just one year ago,” Obama said.

The administration has proposed an overhaul of U.S. financial regulations

including oversight of the systemic risk large financial institutions pose to

the economy, new ways for the government to dismantle failed companies and a

regulator to oversee financial products for consumers.

Obama reiterated his calls for Congress to act on his regulatory proposals,

which he also made in a speech on Wall Street Sept. 13.

“As I told leaders of our financial community in New York City earlier this

week, a return to normalcy can’t breed complacency,” Obama said in today’s

address. “Our government needs to fundamentally reform the rules governing

financial firms and markets to meet the challenges of the 21st century.”

The Financial Crisis Inquiry Commission,

created by Congress to examine the causes of the crisis, held its first public meeting last week. In his opening remarks,

the chairman, Phil Angelides, a former California state treasurer, likened the group’s potential impact to that of the

Pecora hearings in the 1930s, which examined the stock market crash of 1929 and led to transformational changes in banking,

investing and financial regulation.

And yet, last week’s meeting was oddly inauspicious, feeding doubts

about the commission’s ability to realize that potential.

For starters, the meeting was a long

time coming, and thin on substance. It has been four months since Congress passed a law authorizing the commission and two

months since lawmakers selected its 10 commissioners — six chosen by the Democratic leadership and four by the Republican

leadership.

Just days before the meeting, Mr. Angelides announced the hiring of the commission’s

executive director, Thomas Greene, a chief assistant attorney general in California. Mr. Greene has performed ably in various

cases, including those involving antitrust issues against Microsoft and civil prosecutions of Enron. But he will need to hire

tough Wall Street experts to assist him. He may also find himself hobbled by restraints on his subpoena power, because the

commission rules, written by Congress, require that Democrats and Republicans on the commission agree before subpoenas can

be issued.

The meeting itself was mainly prepared statements from commission members, describing the

group’s mission and expressing their commitment to a full investigation. In their more enlightening moments, some of

the commissioners previewed specific concerns to pursue — like the role in the crisis of derivatives, of Fannie Mae

and other too-big-to-fail institutions, and of the Federal Reserve and other regulators.

But

the real work — gathering documents and taking testimony from financial executives and government officials —

will not start before November. Public hearings are not expected until December. A final report is due to Congress on Dec.

15, 2010.

Whenever you find you

are on the side of the majority, it is time to pause and reflect

--- Mark Twain

We have never observed

a great civilization with a population as old as the United States will have in the twenty-first century; we have never observed

a great civilization that is as secular as we are apparently going to become; and we have had only half a century of experience

with advanced welfare states...Charles Murray

Kella

This is a personal website containing personal information and some news and personal opinions on

certain issues affecting democratic governance of interest to me and my friends, associates and seminar participants. The

financial information, charts, etc., consist of items I find interesting. Draw your own conclusions from it.

Copyright Notice: In accordance with Title 17 U. S. C. Section 107,

any copyrighted work on this website is distributed under fair use without profit or payment to those who have expressed an

interest in receiving the included information for nonprofit research and educational purposes only. Ref.: http://www4.law.cornell.edu/uscode/17/107.html